Let us start by learning about depreciation.

What is depreciation? It refers to the value your car parts lose over time due to age, usage, and wear & tear.

The car insurance industry closely monitors depreciation during the claims process. They apply depreciation percentages to the following: plastic, rubber, and metal parts, paint materials, and fibreglass components.

Meaning, if your car is involved in an accident or collision and some of its parts need full replacement, during the claim process, your provider may only pay a portion of the repair cost—the rest you’ll have to shoulder yourself.

Solution? Where there is a problem, there is a way out. Here it comes in the form of zero-depreciation car insurance.

Let us learn more about it …

What is zero-depreciation insurance?

Also known as nil depreciation cover, zero-dep, or bumper-to-bumper cover, it is an add-on coverage to your standard comprehensive car insurance policy.

Often, when a policyholder files a claim for damaged car parts, the insurance company first calculates depreciation. This is done to reduce the claim payout based on parts' wear and tear over time.

Under zero-depreciation coverage, insurance companies do not deduct depreciation from the claim amount. Meaning, once the claim gets approved, you will receive a higher claim payout and pay less from your own pocket.

Let us understand the same with the help of an example -

Say, during an accident, your car’s bumper got damaged, which costs PHP 20k to replace. Without zero-dep coverage, your provider will only pay PHP 12k after depreciation. However, with zero-dep coverage, your insurer will pay the full part replacement amount, i.e, PHP 20k.

Also Read: Car broke down? Here’s how towing can rescue you fast

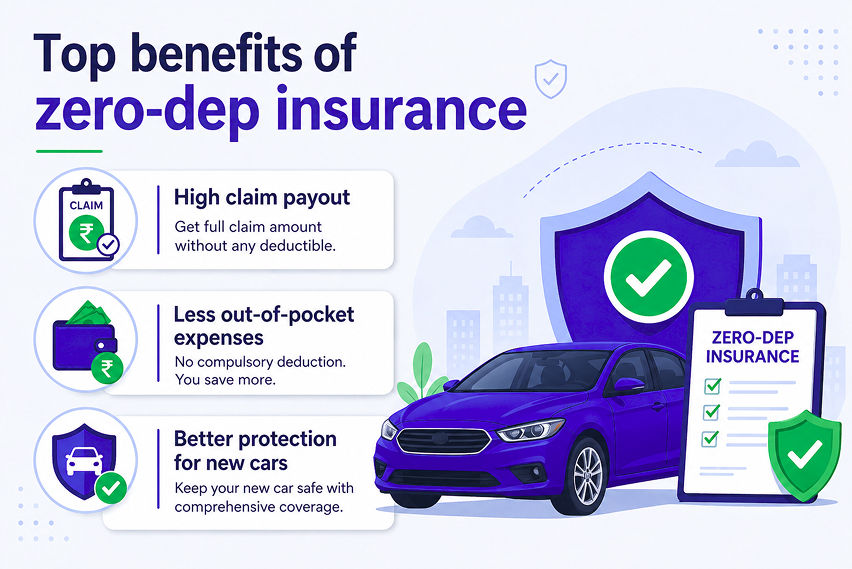

Top benefits of zero-dep insurance

AI-Generated Image

AI-Generated ImageThere is a reason why insurance experts highly recommend zero-dep insurance. Let’s check out its top benefits -

Benefit #1. High claim payout

One of the biggest advantages of a zero-dep add-on is a high settlement amount. Since this coverage waives off depreciation deduction, the policyholder gets better reimbursement for replacement parts. This means fewer surprise expenses, which frankly nobody likes.

Benefit #2. Less out-of-pocket expenses

Without zero-dep coverage, you might pay considerably more during repairs. However, with this add-on, your wallet suffers less.

Benefit #3. Better protection for new cars

If your car is new, fresh out of the dealership, a zero-dep coverage makes all the sense. Why? Well, that’s because new car parts are costly, and depreciation deduction hits hard when your car is still in the wrapper.

Also Read: Top 10 popular car mods - and the ones that raise your premium

Zero-dep insurance: Situations where it might not be for you

Let us be honest: not every car insurance add-on is for you, and the same goes for zero-depreciation coverage. In such cases, it is better to skip that to pay for something that isn’t useful at all.

Here are a few examples of such situations -

You own an old car: If your car is 8 to 10 years old or more, the provider might never offer you zero-dep coverage. Most insurance providers offer it to cars that are 5 years old or less.

You rarely use your car: If the car mostly stays in the garage and rarely hits the road, the risk of an accident/collision is low, making zero-dep coverage unnecessary.

You have a very tight budget: There is no hiding the fact that zero-dep insurance is a bit costly. So, if you are someone living on the edge, you only spend on essential protection. Insurance should not feel like a burden or give you stress.

Cost of zero-dep insurance

The cost of zero-dep insurance depends on several factors, including the car's make & model, location, age, claim history, coverage limit, and provider.

In usual scenarios, zero-dep insurance hikes your premium by 15-30%, which doesn't sound expensive upfront, but compared to the hundreds of pesos paid for accidental repairs, it is nothing.

It could be paying a little now and avoiding a big expense later.

Zero-dep insurance: Aspects to check before policy renewal

When renewing your policy, don’t just go ahead with your existing policy. Rather than checking and comparing a few policies, make a rational decision only after doing so. Here are the details to check for zero-dep insurance.

|

Vehicle age limit |

Many providers have a few age limits for zero-dep insurance coverage. For instance, they offer this coverage for either brand-new cars or cars up to 3 years old, or sometimes up to 5 years old. |

|

Number of claims allowed |

Depending on the provider and policy terms, some plans allow 2 to 3 claims per year. Once all claims are used, coverage benefits may end. |

|

Inclusions & exclusions |

Not every car part may qualify for zero-dep insurance. There are always some exclusions; make sure to always ask for a clear list. We recommend ensuring the coverage includes plastic parts, rubber, tyres, glass, batteries, and fibreglass. |

Also Read: Why do two drivers with the same car pay different premiums?

Common mistakes car owners make (at renewal)

Below, we have discussed a few traps that car owners must avoid at the time of policy renewal -

Renewing without comparing policies: One of the biggest mistakes that you can make as a policyholder is not comparing policies before renewal. You see, different providers offer different coverages, facilities, and terms. Renewing unquestioningly just because it is convenient can cost you in the long run.

Focusing on cheap premiums: Cheapest policy might save you money today, but it could soon prove to be your biggest mistake. Such policies offer poor claim support and minimal coverage, with many terms, which makes the entire deal very expensive later.

Ignoring claim process quality: At the time of need, like an accident, what matters the most is the speed of your claim process. So, never ignore checking this attribute via existing customers and online reviews. While doing so, try to find an answer to the following questions -

- How long does the claim approval process take?

- Is roadside assistance included?

- How extensive is the repair shop network?

Also Read: Smart parking habits that protect your car (and your policy)

Checklist for choosing the zero-dep coverage

Photo from Freepik

Photo from FreepikConfused whether or not to choose zero-dep coverage for your car? Here’s a simple checklist…

Choose zero-dep if -

- You drive daily

- Your car is expensive

- You commute to high-traffic areas

- You prefer peace of mind over anything else

Skip zero-dep if -

- You rarely drive

- Your car is old

- Your budget is a bit tight

- You can manage the repair cost yourself

Tip: The trick is to match your driving and lifestyle with your insurance coverage.

Also Read: The Philippines Insurance Commission: Ways in which it protects car owners

Zero-dep coverage & used cars

It depends on several factors. If the used car is -

- Expensive to repair

- In excellent condition

- Frequently used

- Under the provider’s age limit

… it may be worth getting zero-dep coverage for it. However, if your pre-loved car is old and its repair cost is manageable, standard insurance may be enough.

Remember, be rational. Your goal here is to choose practical protection rather than unnecessary spending.

Also Read: When your car insurance won’t help you - even if you paid on time!

Bottom line

It is crucial to understand the services you are paying for, so that later, when the need arises, you can use them to their full potential. The same is the case with car insurance; you need to understand the coverages before starting to pay. However, the issue is which coverage to opt for (as per your driving requirements) so that you don’t end up over- or underinsured.

The one car insurance add-on we feel most car owners would appreciate after an accident is zero-depreciation coverage. So, if you don’t already have this coverage and your policy is due for renewal soon, this article is a must-read.

You see, Filipino car owners focus mainly on the premium and pay minimal attention to the most important aspect of insurance, i.e., ‘how much will I pay for repair in case of an accident/collision?’

It is here that zero-depreciation coverage comes into play; though it is not the cheapest option, it is surely the smartest one, especially if your car is new, frequently used, and expensive to repair.

Before proceeding with the renewal process, pause, ask questions, compare policies, and read the fine print.

Also Read: Personal Accident Coverage for riders in the Philippines: Why it matters

FAQs

Q1. How many times can I claim zero-dep insurance benefits?

Ans. The answer to this question depends on your provider and policy terms. In most cases, a policyholder can make 2 to 3 claims annually. We recommend confirming the policy limits with your provider.

Q2. Are scratches and dents covered under zero-dep insurance?

Ans. Yes, but only if they are part of the accidental damage claim and meet all the policy terms & conditions.

Q3. Can zero-dep coverage be added at renewal?

Ans. Yes, in fact, many policyholders opt for zero-dep coverage at renewal after reviewing their needs or following a disappointing claim experience.

Q4. Can I get zero-depreciation coverage for my used car?

Ans. Yes, but given that your used car meets the insurer’s requirements, which mainly concern the car’s age and condition.

Q5. Why is zero-dep coverage expensive compared to other add-ons?

Ans. Well, that’s because under the zero-dep claim, the insurer faces higher claim payouts, which results in a higher premium.

Q6. Is zero-dep insurance worth it for first-time car owners?

Ans. Absolutely, especially if the car owner requires strong financial protection against accidental damage.

Q7. Is engine damage covered under zero-dep coverage?

Ans. Not necessarily. You see, engine coverage depends on the insurance policy and the cause of damage. For instance, flood-related engine damage often requires separate coverage.

Q8. Is zero-dep coverage available for all car owners?

Ans. Insurance providers usually offer zero-dep coverage to new vehicles, usually under 3 to 5 years old.

Q9. Is zero-dep a replacement for comprehensive coverage?

Ans. Not at all. You see, zero-dep coverage is an add-on to comprehensive coverage and not a replacement for it.

Q10. How does a policyholder get a higher claim with zero-dep coverage?

Ans. In case of a zero-dep coverage claim, the insurer does not deduct depreciation on replaced parts, giving policyholders a higher payout.

Also Read: Is your current insurance provider still worth it in 2026? Here’s how to tell