Running a business is no joke, especially in today’s economy. You need to manage a fleet of delivery vans or service trucks, handle drivers, control fuel costs, meet deadlines, and all this is often under the scorching sun.

And when the monsoon hits, the situation becomes even more complicated: stress, delays, and financial risk all increase at once.

Most business owners assume that paying premiums and keeping paperwork in order keep their fleet safe.

But standard policies have massive blind spots—traps and clauses that let insurers completely reject claims. When a rainstorm floods your depot or stalls multiple trucks, being left unsupported can be a total nightmare, sometimes enough to sink a small business.

With these risks in mind, it's important to consider how and where local businesses can get caught off guard during the monsoon season. Here’s how you can protect your hard-earned money and business before the skies open up again.

Also Read: Build better insurance coverage for your business vehicle in 2026: 9 smart strategies to know

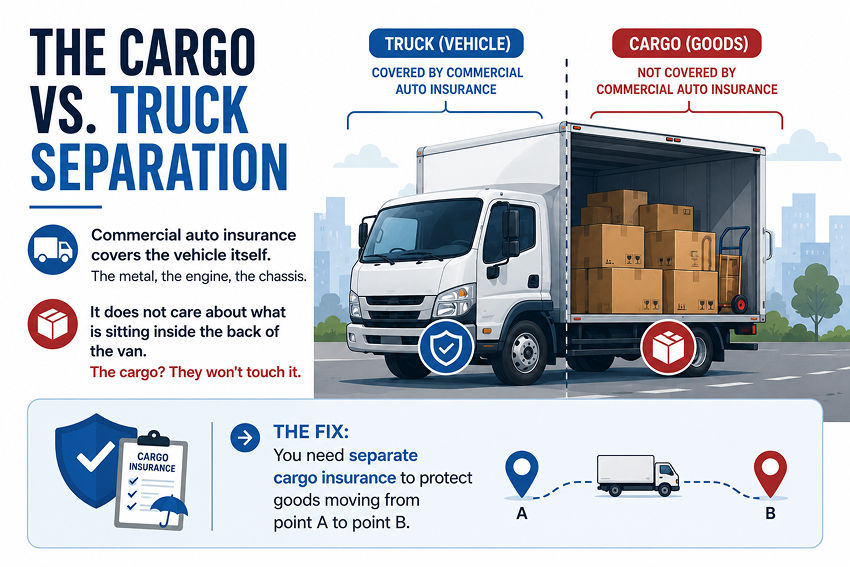

1. The cargo vs. truck separation

AI-Generated Image

AI-Generated ImageThis catches so many logistics and retail businesses completely by surprise. Your commercial auto insurance covers the vehicle itself. The metal, the engine, the chassis. It does not care about what is sitting inside the back of the van.

If a flash flood traps one of your delivery vehicles and ruins PHP 500,000 worth of customer orders or electronic stock inside, your standard fleet policy will only pay to fix the truck. The cargo? They won't touch it.

The Fix: You need separate cargo insurance to protect goods moving from point A to point B. Without it, your inventory will be at risk every time.

Also Read: Truck/Commercial Vehicle Insurance 101: What Filipino business owners need to know

2. The pressure to deliver goods vs. negligence

A driver, under pressure to meet the delivery timeline, encounters a flooded street. Instead of turning back, which could cause delays and negative feedback, he proceeds. This decision leads to engine damage from water intake, resulting in significant losses. The engine, the pistons seize, and the motor is destroyed.

To a Philippine insurance company, this isn't a covered accident. It’s gross negligence.

Major local auto insurers say if a driver braves deep water despite flood warnings, the claim can be denied. Their argument: the damage was caused by avoidable human choices, not just by weather.

A real word of advice: Sit your drivers down. Make it a strict company rule that they must stop and reroute if water rises past the centre of the wheels. Protect your people, and protect your engines, because the insurer won't cover impatience.

Also Read: Why every truck business needs Comprehensive Truck Insurance in the Philippines

3. When your fleet is fine, but stuck

Sometimes, the storm doesn't touch your trucks at all. Instead, it floods the main road leading out of your warehouse. Or the power goes out for days, leaving you unable to run your loading bays. Your fleet is perfectly functional, but completely stuck.

You lose money every single hour those wheels aren't turning.

Standard fleet insurance only applies if there’s physical damage to the vehicle. If trucks are fine but operations stall due to weather, a basic auto policy offers no financial relief.

The fix: It's worth talking to a broker about insurance covers that help cover your fixed costs, like employee salaries, when a natural disaster forces you to hit the pause button.

Also Read: Most overlooked commercial vehicle insurance add-ons for 2026: A helpful guide for vehicle owners

4. One parking spot for your whole fleet

AI-Generated Image

AI-Generated ImageWhere do your vehicles sleep at night? If you park your entire fleet in a single yard or underground warehouse, you centralise all the risk at that location. One bad night of rain can wreck multiple company assets at once.

Like personal car insurance policies, commercial plans require an add-on for natural disasters, called Acts of God or Acts of Nature. This usually increases the premium. If your broker missed this for any vehicle, flooding can mean paying for a new fleet yourself.

Also Read: Top 7 risks covered by truck and commercial vehicle insurance

Bottom line

At the end of the day, commercial vehicle insurance is an essential safety net, but it only works if you actually know where the netting is lost or torn. The real secret to surviving the monsoon season isn't just buying a policy; it’s pairing that paperwork with real, active care.

Take a look at your policy schedules this week. Make sure "Acts of God" coverage applies to every vehicle you own, and keep a digital folder on your phone with all your policy numbers and claims hotlines.

Combine that paperwork with basic fleet maintenance. Check tyre treads weekly so your drivers don't hydroplane, replace those streaky old windshield wipers, and give your team the explicit authority to delay a delivery if a road looks like a river. A delayed order might annoy a customer for an hour, but a rejected insurance claim and a ruined engine can cost you the whole business.

FAQs

Q1. Does commercial fleet insurance automatically cover typhoons and floods?

Ans. No, it really doesn't. Standard commercial auto insurance usually covers only basic accidents, theft, and third-party liability. Damage from typhoons, floods, or landslides is covered by a specific add-on called Acts of God or Acts of Nature. You have to check your policy schedule to confirm this is active for every vehicle.

Q2. If my driver gets stuck in a storm, will the insurance pay for towing?

Ans. Only if your policy explicitly includes a commercial roadside assistance add-on. Don't assume it’s there just because it’s a business account. Also, many standard roadside plans have weight limits, so if you operate large trucks, you need to make sure your towing coverage actually matches the size of your fleet.

Q3. What is a digital "Claims Kit" and why should a business make one?

Ans. It’s basically just a secure folder on Google Drive, Dropbox, or your phone containing copies of all driver's licenses, vehicle registrations (OR/CR), insurance policy numbers, and company claims hotlines. When a storm knocks out your office power or internet, you or your managers can still file claims immediately on your phones, putting your business at the front of the line for repairs.

Q4. Can an insurer really deny a business claim if our driver drove through a flood?

Ans. Yes, insurers can deny a claim if they can prove gross negligence or that the driver intentionally drove into danger, which caused the engine to flood. The insurer will argue the damage was totally avoidable and reject the payout.

Q5. Are the tools and equipment inside our company vehicle covered?

Ans. Generally, no. Standard commercial auto insurance treats tools, laptops, and specialised gear inside the vehicle as personal property or loose cargo. To protect the valuable equipment your team/driver uses on the road, you’ll need a separate coverage/policy.

Q6. How is the participation fee calculated if multiple fleet vehicles are damaged?

Ans. The participation fee or deductible is the out-of-pocket amount your business must pay before the insurance company covers the remaining repair costs. In the Philippines, this is usually calculated per vehicle, although the exact terms depend on the insurer and policy.

Also Read: Common costly mistakes to avoid when filing a commercial vehicle insurance claim