You’ve probably already mapped out your dream itinerary: eating authentic ramen in a hidden Tokyo alley, taking photos with the deer in Nara, or catching the stunning cherry blossoms in Kyoto. You have your clothes packed, your budget tracking sheet ready, and you are counting down the days until your flight.

But as you review everything for the one last time, a thought takes over the excitement: Do I need travel insurance? Is it a mandatory requirement for Filipino tourists entering Japan?

We know that navigating visa rules and entry protocols can feel quite overwhelming. To clear up the confusion, we have created this guide. It breaks down the following: official rules on Japan travel insurance requirements for Filipino passport holders, why skipping it is a massive gamble, and how to pick the right plan without overspending.

The official rule: Is travel insurance mandatory for a Japan visa?

Also Read: Flight Delayed? How travel insurance can save your dream road trip

Let’s get the legalities out of the way first

The official stance: No, travel insurance is not a strict or mandatory requirement for securing a Temporary Visitor Visa (tourist visa) from the Embassy of Japan in the Philippines. You will not be denied a visa simply because you didn't attach an insurance certificate to your application at the visa centre.

However, there is a massive catch. Both the Japan National Tourism Organisation (JNTO) and the Philippine Embassy in Tokyo strongly advise and explicitly recommend that all incoming tourists secure comprehensive international travel medical insurance before flying.

While immigration won’t turn you away at the border for lacking a policy, travelling without one leaves you completely exposed to Japan’s complex and incredibly expensive healthcare system.

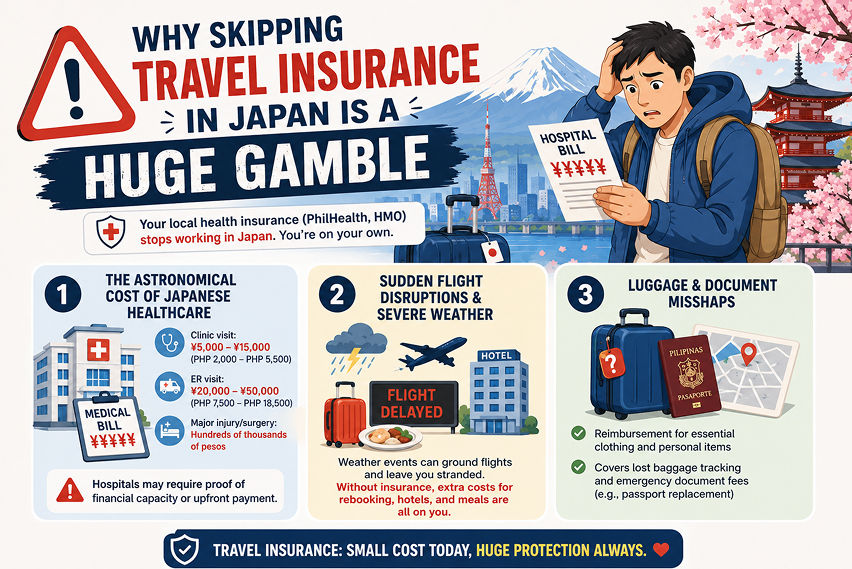

Why skipping travel insurance in Japan is a huge gamble

When you visit Japan, your local health insurance, such as PhilHealth or your company HMO card, stops working. If an emergency happens, you are entirely on your own.

Also Read: Travelling with kids? Don't skip these travel insurance tips

Here is why having a robust insurance policy is practically essential when exploring the Land of the Rising Sun:

1. The astronomical cost of Japanese healthcare

Japan boasts world-class medical facilities, but for uninsured foreigners, it comes with a premium price tag. Tourists have to pay 100% of all medical costs upfront.

A basic clinic visit for food poisoning or a severe cold can cost ¥5,000 to ¥15,000 (about PHP 2,000 to PHP 5,500).

An emergency room visit can easily cost ¥20,000 to ¥50,000 (PHP 7,500 to PHP 18,500).

If you suffer a major fracture while skiing in Hokkaido or need an emergency appendectomy, the bill can easily climb into hundreds of thousands of pesos.

Many Japanese hospitals will require proof of financial capacity or an upfront payment before admitting non-emergency patients.

AI-Generated Image

AI-Generated Image2. Sudden flight disruptions and severe weather

Japan is beautiful, but it is also prone to natural disasters, including severe winter snowstorms and summer typhoons. If a weather event grounds all flights out of Tokyo Narita, you could find yourself stranded. Without insurance, the costs of rebooking your flights, paying for extra nights you stay at a hotel, and buying meals will fall entirely on your pocket.

3. Luggage and document mishaps

Imagine arriving at the airport in Japan only to find your suitcase containing all your winter gear is missing. Or worse, you accidentally lose your passport while exploring the crowded streets of Shibuya. A good travel policy reimburses you for the purchase of essential clothing. At the same time, your bags are tracked down, and it covers the steep administrative fees required to secure emergency travel documents from the Philippine Embassy.

Also Read: Maximising your peace of mind: Traveller's guide to Hong Kong travel insurance

What a good Japanese travel insurance plan must cover

Since Japan is a high-cost medical destination, a generic, cheap insurance plan might not cut it. When comparison-shopping for a travel policy, ensure it checks these specific boxes:

- High medical coverage limits: For a trip to Japan, do not settle for a basic PHP 500,000 limit. Aim for a policy that offers PHP 2,000,000 or higher in emergency medical expenses to ensure you are fully protected against major hospital bills.

- Cashless claim capabilities: Look for digital-first providers that offer cashless assistance. This means that if you get sick, the insurer coordinates directly with the network hospital to handle the bill, so you don't spend your personal savings.

- Hazardous sports coverage: If your itinerary includes hitting the ski slopes, make sure your policy explicitly includes the required add-on. You see, standard base policies often treat skiing and snowboarding as high-risk exclusions.

- Trip interruption and cancellation: This protects your prepaid, non-refundable hotel stays and activity bookings if a family emergency or a sudden, severe illness forces you to cancel the trip.

Conclusion: Travel with true peace of mind

Planning a trip to Japan? If so, it is an incredible experience, but true smart travel means being prepared for the unexpected. While the Japanese government won't force you to show a policy at the immigration desk, securing comprehensive travel insurance is the smartest financial decision you can make.

For less than the cost of a single plate of premium dinner, you can protect your hard-earned savings, secure 24/7 expert medical assistance, and even ensure that a sudden travel mishap doesn’t turn your vacation into a financial nightmare. It only takes five minutes to get covered before you fly, just do that and enjoy everything that Japan has to offer with complete peace of mind!

Also Read: Travel insurance FAQs for 2026: Everything travellers most commonly ask

FAQs

Q1. Can I use the complimentary travel insurance from my credit card for Japan?

Ans. Some premium credit cards offer free international travel insurance when you use their card to purchase your round-trip flights. However, you must read the fine print. Many of these free card coverages carry high deductibles, low medical maximums, or exclude winter sports entirely. If the coverage is weak, it is safer to spend a few hundred pesos on a dedicated standalone policy.

Q2. Does budget travel insurance cover earthquakes or tsunamis in Japan?

Ans. Comprehensive policies do cover natural disasters, provided the policy was purchased before the disaster became a known event. It is recommended to check your policy's exclusion list and keep an eye on local weather and safety alerts before departing.

Q3. When is the best time to purchase my policy?

Ans. It is recommended to get your travel insurance policy after booking your flights and hotels. The trip cancellation benefit only protects you against events that occur after you buy the policy. Purchasing it weeks in advance ensures your investment is shielded from early disruptions.

Q4. I feel sick while travelling in Japan. What shall I do?

Ans. Contact your insurance provider's 24/7 emergency hotline immediately. They will guide you to the nearest accredited English-speaking clinic or hospital and explain whether your treatment can be processed as a cashless claim.

Q5. My luggage was lost at a Japanese airport. How do I file a claim?

Ans. You must file a report before leaving the baggage claim area and secure a physical copy of the Property Irregularity Report (PIR) from the airline staff. Your insurance provider requires this document to process any baggage loss or delay claims.

Also Read: Decoding the fine print: A Pinoy guide to travel insurance policies