We all know the drill. One minute you’re baking under the midday Manila sun, and the next moment, the sky turns purple and drops a literal ocean onto EDSA. Welcome to the rainy season in the Philippines.

While some worry about the laundry drying indoors or whether the wipers will survive the next downpour, there’s a massive financial trap hiding in plain sight: your car insurance. Most people assume that with comprehensive insurance by their side, they’re covered for everything. But, they aren't.

So, before the next tropical storm turns your daily commuter into a makeshift boat, run through this quick, honest car insurance checklist.

Also Read: The Philippines Insurance Commission: Ways in which it protects car owners

1. Confirm you have "Acts of Nature" (AON) add-on

Let’s bust the biggest myth right now. Standard comprehensive car insurance does not automatically cover flood damage.

If a typhoon submerges your sedan in the parking lot, or a falling tree branch crushes your roof during a TCWS (Tropical Cyclone Wind Signal) No. 3 storm, basic insurance will look the other way. You need Acts of Nature (AON), sometimes called Acts of God.

Check your policy schedule: Look for the specific line item that says "Acts of Nature" or "AON."

The cost: It usually adds about a fraction of a per cent—around 0.5% to 0.75% of your car's total insured value. Is it worth it? Absolutely. Especially if you live in low-lying parts.

If you don’t see it on your papers, call your agent today. Don't wait for the government to name the next typhoon. By then, it will be too late to add coverage.

Also Read: Got a new high-end car? Here is the best insurance guide (for 2026)

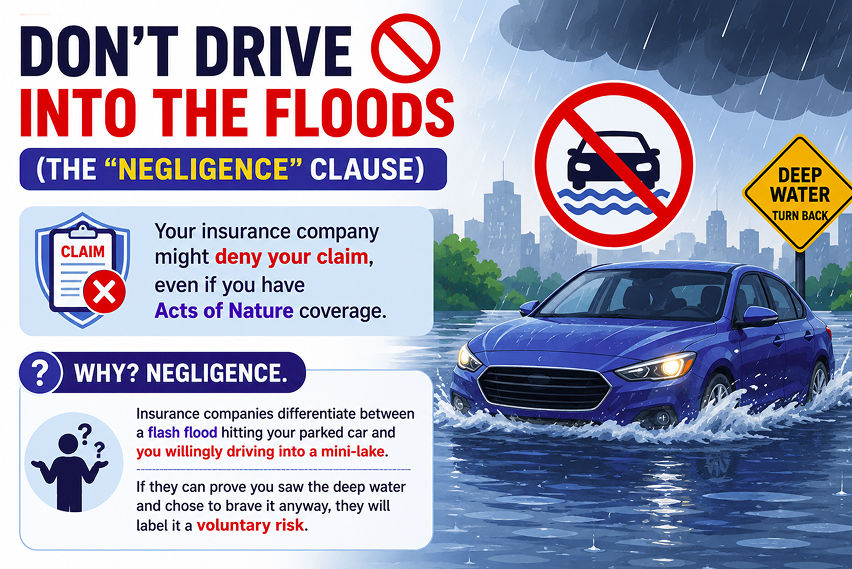

2. Don't drive into the floods (the "Negligence" clause)

AI-Generated Image

AI-Generated ImageYou’re driving home. It’s pouring. You hit a flooded street, look at the gutter, and think, “I can make it.” You step on the gas, the engine sucks in water, and the car dies. Hydro-lock.

Here is the brutal truth: your insurance company might deny your claim, even if you have Acts of Nature coverage.

Why? Negligence. Insurance companies differentiate between a flash flood hitting your parked car and you willingly driving into a mini-lake. If they can prove you saw the deep water and chose to brave it anyway, they will label it a voluntary risk.

Rule of thumb: If the water is higher than half your wheels, turn back. No meeting or dinner is worth the engine-rebuild cost you have to pay out of pocket.

3. Dig up your emergency roadside assistance hotline

Getting stuck in the middle of a heavy downpour is stressful enough. And trying to find a reliable tow truck while your mobile data is dropping bars in the middle of a storm is a whole other hell.

Most comprehensive insurance policies include 24/7 roadside assistance.

Make sure to -

- Save the number: Don't leave the insurance/roadside assistance booklet in the glove compartment. Take a photo of the hotline number and save it in your phone contacts under "Car Insurance Towing."

- Know the limits: Check whether the provider offers free towing up to a certain distance or charges extra beyond that.

Also Read: 9 shocking total loss coverage myths every car owner should stop believing

4. Prep your digital claims kit

AI-Generated Image

AI-Generated ImageIf the worst happens and your car gets waterlogged or dented in a rainy-day mishap, you’ll need to file a claim fast. The lines get long after a big storm.

Keep digital copies of these essentials on your phone or cloud storage:

- Your updated Driver’s License and Official Receipt (OR/CR)

- Your current insurance policy

- The contact details of your insurer’s claims department

If you are thinking of filing a claim and want it to pass, make sure to take photos of everything immediately. This includes the water level, the damage, the surrounding landmarks, everything. Do it before the car gets moved.

Also Read: 2026 guide for car insurance claim documents - A must-read

Bottom line

Look, at the end of the day, insurance is just a safety net. It’s there for the absolute worst-case scenarios, but it shouldn't be your only line of defence. The real secret to surviving the rainy season is pairing proper coverage—like making sure "Acts of Nature" is actually ticked on your policy and saving that roadside assistance hotline—with some basic, proactive car care.

Take five minutes this weekend to check your tyres so you don't hydroplane on the highway. Finally, replace those streaky, useless wiper blades. Having your digital claims kit ready on your phone is great, but avoiding the mess entirely is always better.

And remember, don't let recklessness ruin your safety net; driving straight into a flooded street out of impatience is a form of negligence that will get your claim denied. Just peek at the weather apps before you grab your keys. Stay safe out there. The roads get pretty brutal this time of year, and no shortcut is worth a destroyed engine.

Also Read: Common myths about ‘Acts of Nature’ coverage debunked

FAQs

Q1. What exactly is a participation fee, and will I have to pay it for flood damage?

Ans. The participation fee, also known as a deductible, is the amount you agree to pay out of pocket before the insurance payout kicks in. Even if a typhoon floods your car and you have Acts of Nature coverage, you will still need to pay this fee. It is usually a small percentage of your car's value.

Q2. Can I buy Acts of Nature coverage on its own if I only have CTPL?

Ans. Unfortunately, no. Compulsory Third Party Liability (CTPL) only covers bodily injury or death to third parties. To get Acts of Nature coverage, you must have a comprehensive car insurance policy first, then add AON as an optional rider.

Q3. My car got flooded while parked in my office basement. Who pays?

Ans. If you have Acts of Nature coverage, your car insurance company should cover it. However, if the building management was explicitly negligent, like their flood pumps failed due to poor maintenance, your insurance company might pay you first, then go after the condo administration to recover the money.

Q4. What should I do immediately if water starts rising inside my car?

Ans. Prioritise your life over the machine. If the water is rising fast, turn off the engine to minimise internal damage, grab your valuables, leave the car, and get to high ground. If the car is already submerged, do not try to start it after the water recedes. Starting a waterlogged engine can destroy it, turning a fixable problem into a total loss.

Q5. Does insurance cover my phone or laptop if they get ruined in a flooded car?

Ans. Standard car insurance only covers the vehicle itself and its factory-installed parts. Personal items left inside the car—like laptops, bags, or smartphones—are generally not covered under your auto policy. Some comprehensive policies include "personal item/effects" coverage, but the limit is usually quite low.

Q6. How long do I have to file an insurance claim after a storm?

Ans. Most insurance companies in the Philippines require you to report the incident as soon as possible, preferably within 24 to 48 hours. Don't wait. After a major typhoon, insurance hotlines and adjusters get completely overwhelmed. The sooner you file your report and submit your photos, the sooner you'll get into the repair queue.

Also Read: From rejection letter to payout: How to successfully appeal your car insurance claim