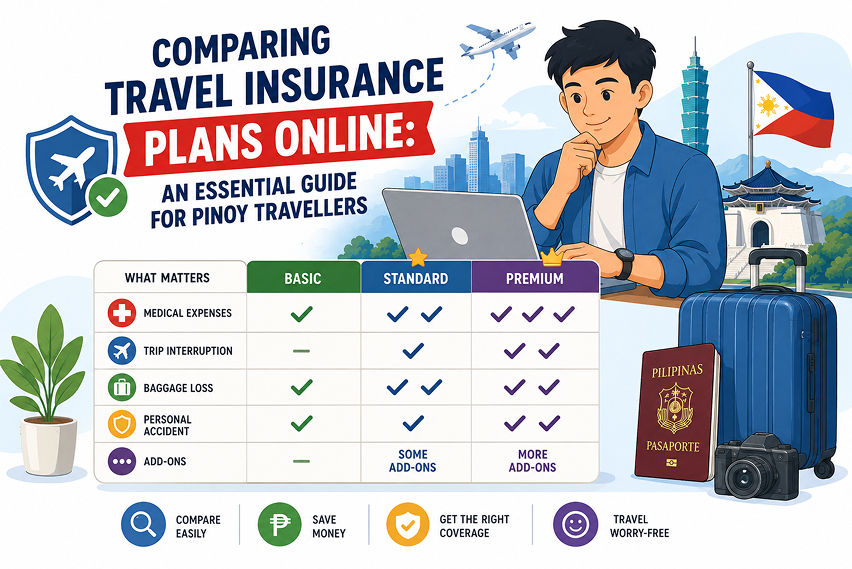

Planning is the most stressful and important part of a vacation. Choosing which beach to lounge on. Mapping out the best night markets. Listing cool eating and shopping spots.

But when it comes to adding travel insurance, most of the time, Filipinos just say ‘No’ without even thinking. Why? Well, there are so many rumours and myths floating around about travel insurance. Many people think it's just a trick for airlines to make extra money.

Also Read: What is travel insurance, and why every Filipino traveller should understand it

Let's clear the air and look at the most common travel insurance myths that Filipinos still believe—and why they are totally wrong.

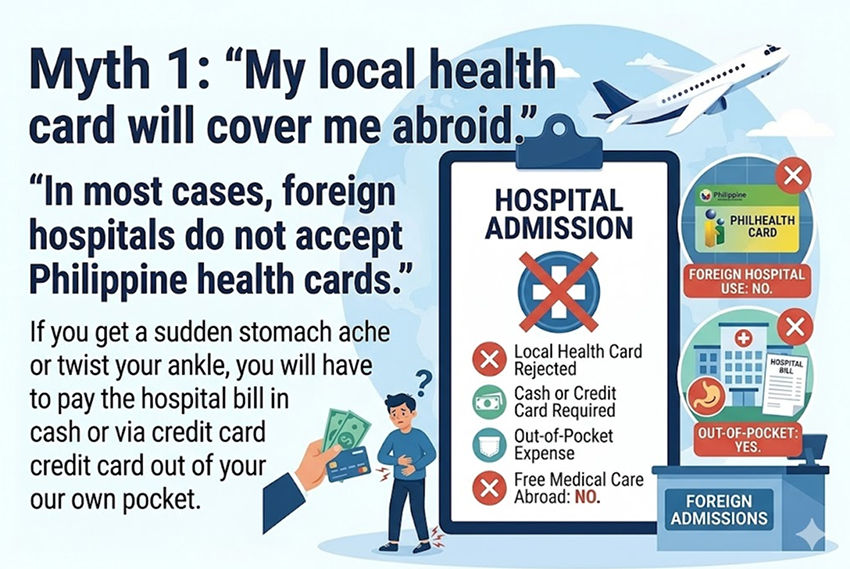

Myth 1: "My local health card will cover me abroad."

AI-Generated Image

AI-Generated ImageThis is the biggest mistake people make. You might have a super fancy Maxicare, Medicard, or PhilHealth card from your job in the Philippines, which makes you feel safe.

But guess what? The moment your plane lands in Singapore, Japan, or the US, those cards are pieces of plastic.

In most cases, foreign hospitals do not accept Philippine health cards. If you get a sudden stomach ache or twist your ankle, you will have to pay the hospital bill in cash or via credit card out of your own pocket. Hospital bills in those places can easily cost PHP 100,000 or more for a single night!

Travel insurance is what actually covers those scary bills while you are in another country.

Myth 2: "Travel insurance is way too expensive."

AI-Generated Image

AI-Generated ImageWhen people hear the word travel insurance, they think of thousands of pesos. They think it's only for rich families.

Actually, it is incredibly cheap.

If you are just flying to a nearby country like Thailand or Hong Kong for a five-day vacation, a basic travel insurance plan from a trusted local provider (like Oona, Starr, or PGA Sompo) can cost as little as PHP 300 to PHP 500. Spending such a small amount to protect yourself from a PHP 200,000 hospital bill is an amazing deal, right?

Myth 3: "I can just buy it at the airport if things look bad."

AI-Generated Image

AI-Generated ImageImagine you get to the airport and see on the news that a massive typhoon is approaching. You suddenly get scared and try to buy travel insurance on your phone while waiting at the gate.

Sorry, but it will not work.

Insurance companies have a strict rule: you must buy the policy before an emergency occurs or a storm is officially named. Once the problem is already alive and happening, it is too late. You also cannot buy it if you have already left the Philippines. You have to get it while you are still sitting at home planning your trip.

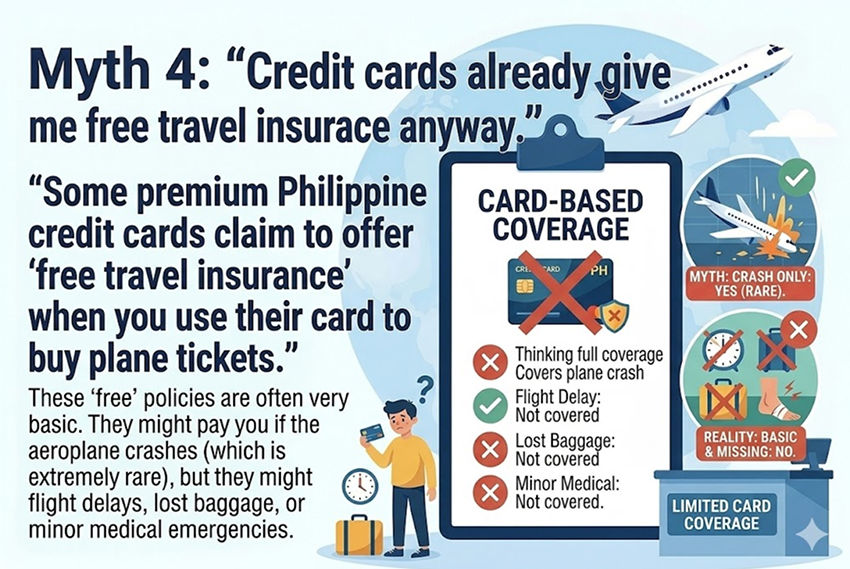

Myth 4: "Credit cards already give me free travel insurance anyway."

AI-Generated Image

AI-Generated ImageSome premium Philippine credit cards claim to offer "free travel insurance" when you use their card to buy plane tickets. It sounds amazing.

But you have to be very careful.

These "free" policies are often very basic. They might pay you if the aeroplane crashes (which is extremely rare), but they might completely skip over flight delays, lost baggage, or minor medical emergencies. Therefore, it is always recommended to read the fine print. Often, buying a standalone policy gives you ten times more protection than the free card benefit.

Myth 5: "I only need insurance for long, international flights."

AI-Generated Image

AI-Generated Image"I am just going to Hong Kong for three days! Why waste money?" or "It's just a domestic flight to Boracay!"

Here is the truth: bad luck does not care how long your flight is.

You can lose your luggage on a 45-minute flight just as easily as on a 14-hour flight. You can get food poisoning from a street food stall on day one of a weekend getaway. A short trip does not magically protect you from mishaps.

The big takeaway

At the end of the day, travel insurance isn't a scam to take your money. It's the ultimate safety net. It ensures that if your flight gets messed up, your stomach acts up, or your bags go missing, your hard-earned vacation savings won't go with them. Don't let old myths ruin your next big adventure.

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

FAQs

Q1. Does the law require Filipinos travelling abroad to have travel insurance?

Ans. In most countries, such as Singapore, Malaysia, or Hong Kong, it is not legally mandatory, but still strongly recommended. However, if you are visiting European countries (the Schengen Area), you are legally required to present a travel insurance policy with at least €30,000 in medical coverage to obtain a visa.

Q2. Can I compare different insurance plans to find the cheapest one?

Ans. Yes! You don't have to just stick with whatever the airline offers you. Websites like ZenInsure let you compare different insurance companies in the Philippines side-by-side so you can choose the exact price and coverage that fits your budget.

Q3. I changed my mind and cancelled my trip. Will my travel insurance cover me?

Ans. No. Standard travel insurance only pays out if you cancel your trip for serious, unavoidable reasons, such as you or a family member becoming seriously ill or a natural disaster shutting down the airport. You can't claim money back just because you don't feel like flying anymore.

Q4. What happens if my flight gets delayed? How does insurance help?

Ans. If your flight is delayed for a long time, your insurance will provide an allowance for food at the airport or for a hotel room if you need to stay overnight. Just remember to ask the airline for proof.

Q5. Are dangerous activities like scuba diving or skydiving covered by standard plans?

Ans. Usually, no. Standard, cheap travel insurance policies explicitly exclude high-risk activities or extreme sports. If you plan to engage in activities such as scuba diving or bungee jumping abroad, you need to purchase a special add-on to your policy.

Q6. Can I buy one travel insurance plan that covers my friends travelling with me?

Ans. You can buy a "Group Plan" or "Family Plan". This allows one person to pay for everyone on the same trip, which is often much faster and sometimes even cheaper than buying separate individual policies for every friend.