Before discussing the common myths about total loss coverage, it is important to outline the protection plan briefly. Coz let’s face it, most car owners know CTPL insurance and a bit about comprehensive insurance.

So, what is total loss? In the world of car insurance, a vehicle is considered ‘total loss’ when its repair costs are more than its actual market value. The vehicle gets labelled as a ‘Constructive Total Loss’ once fixing it hits the 70-80% threshold of its market worth, instead of requiring a full 100%.

How do insurance providers determine total loss? Insurance providers determine total loss by evaluating factors such as the car's current market value, depreciation, age, and repair estimates. By understanding this valuation process, car owners will know why their vehicle may be declared a total loss.

Also Read: When your car insurance won’t help you - even if you paid on time!

Let us now start to discuss the myths surrounding the total loss coverage -

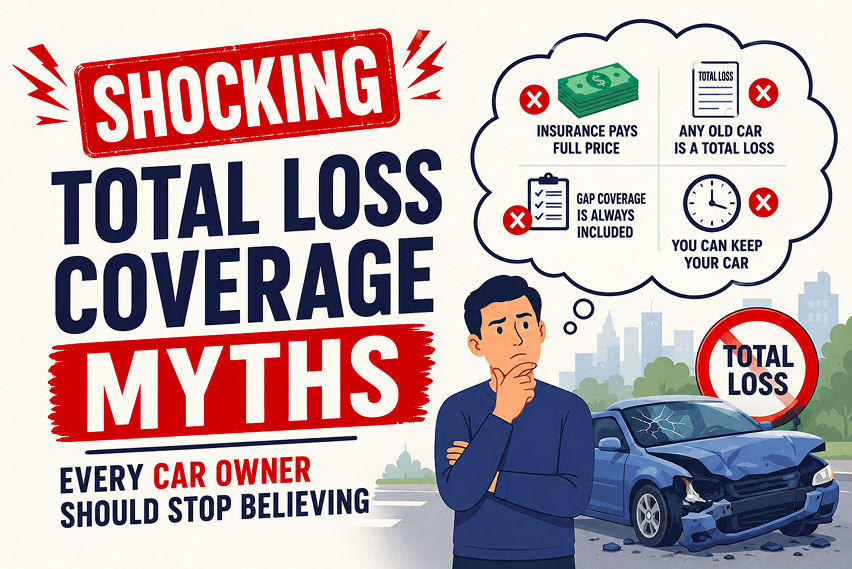

Myth #1: Total loss coverage will pay for the new car

This one is actually funny and is one of the most common misconceptions. You won’t believe how many Filipino car owners think insurance will replace their old vehicle with a brand-new model after a total loss. Sorry to inform you that’s not how things work.

So, what's the deal? Insurance companies usually pay the Fair Market Value of your car. This means: Car Value = Original Price – Depreciation.

That’s why understanding depreciation is critical.

Myth #2: Your insurance policy covers 100% of everything

Many people believe that having a comprehensive insurance plan means “everything is covered.” Unfortunately, there are limitations.

So, despite having insurance, you may still need to pay for:

- Participation fees

- Deductibles

- Depreciated parts

- Processing fee

- Excluded damages

Always review your policy carefully before signing.

Also Read: Personal Accident Coverage for riders in the Philippines: Why it matters

Myth #3: Flood damages are automatically covered

Flooding is a major concern for car owners, all thanks to typhoons and heavy rains. But here’s the truth: flood damages are not always included in standard comprehensive insurance.

You need acts of nature coverage in your policy to get protection from flood damage. This add-on protects against:

- Floods

- Typhoons

- Earthquakes

- Volcanic eruptions

Without this add-on, your insurer may reject flood-related total loss claims.

Myth #4: Old cars don’t get total loss coverage

Some drivers assume insurance companies completely reject older vehicles, but that’s not always the case.

What are the insurance options for older vehicles? It is definitely a challenge to find complete coverage for older cars. Still, many insurers offer quite good deals, provided the vehicle is well-maintained, has passed inspection, and its spare parts remain available. However, premiums for such cars may be higher, and coverage options may be limited.

If you own an older vehicle, it is recommended that you compare multiple providers rather than assume you do not qualify for coverage.

Also Read: Is your current insurance provider still worth it in 2026? Here’s how to tell

Myth #5: Total loss claim approval is quick

Social media often tends to glorify things and even makes the claim process look quick and effortless. But the reality can be very different.

Common reasons why claims get delayed

AI-Generated Image

AI-Generated ImageClaims may take weeks or even months to get processed. Why? Here are a few potential reasons -

- Missing/incomplete documents

- Ongoing investigations

- Police report verification

- Repair estimate disputes

- Ownership transfer issues

Wanna avoid delays? Try these hacks

- Make sure to submit complete paperwork

- Keep copies of all documents

- Respond quickly and truthfully to the insurer

Remember, patience and preparation matter.

Myth #6: It is okay to ignore policy fine print

Most policyholders skip reading insurance contracts because they look too long and complicated—a big mistake. Carefully reviewing your policy from the start helps you understand what is and isn't covered, preventing surprises during claims. For example, some policies exclude damage caused by driver negligence or by unauthorised drivers.

- Driving under the influence

- Unauthorized drivers

- Illegal racing

- Commercial use

- Negligence-related damage

Always read your policy thoroughly before paying premiums.

Also Read: Planning to renew your car insurance policy? Read this zero-dep guide first

Myth #7: Total loss coverage is expensive

Some car owners avoid comprehensive insurance, thinking that it is unaffordable. But compared to replacing a vehicle, paying for insurance is much cheaper.

Affordable ways to stay protected with insurance

- Increase policy deductibles

- Comparing multiple insurers

- Bundle your policies

- Maintaining a clean driving record

- Installing anti-theft devices

Myth #8: Car modifications are fully covered

Car enthusiasts and young drivers in general do not shy away from customising wheels, audio systems, body kits, engine upgrades, etc. But do you know that undeclared modifications can create serious claim problems?

It is very important to inform your provider of any vehicle modifications. Insurance companies need documentation for:

- Custom rims

- Expensive sound systems

- Lift kits

- Turbo upgrades

- Exterior modifications

If upgrades are not declared, insurers may refuse reimbursement for modified parts. Therefore, it is recommended to inform your provider of any changes.

Also Read: Must-have add-ons for 2026: What you shouldn’t miss

Myth #9: Insurance providers undervalue cars

It is a general misconception among car owners that insurers intentionally offer low payouts. While disagreements do happen, valuation by providers is usually the product of an established system. Let’s see how valuation really works, starting with the factors insurance companies often consider:

- Vehicle’s market resale value

- Car’s condition

- Comparable listings

- Depreciation schedules

If there is a disagreement with the valuation. Here’s what you can do -

- Request a detailed breakdown

- Provide maintenance records

- Show comparable market listings

- Seek independent appraisals

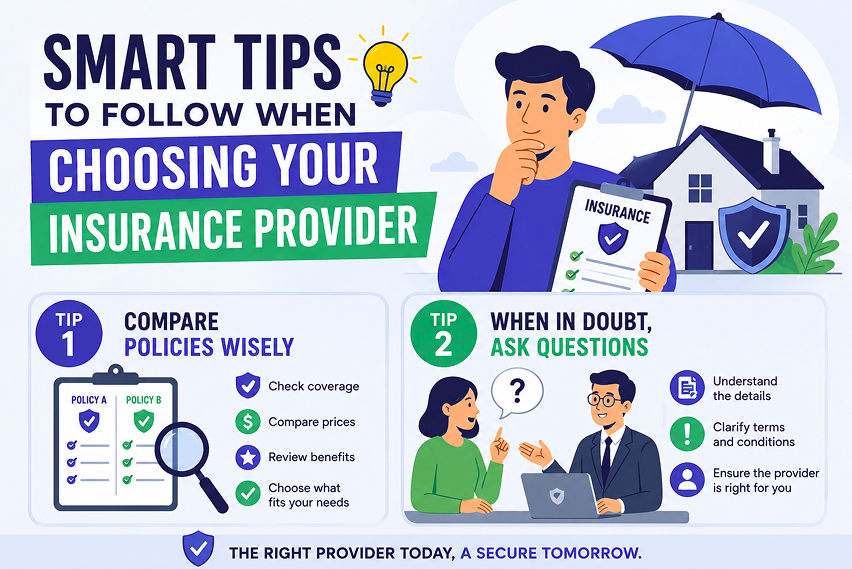

Smart tips to follow when choosing your insurance provider

AI-Generated Image

AI-Generated ImageWith the right insurance provider by your side, you can avoid the stress that comes your way during/after an accident/unfortunate event. Here’s what needs to be done -

Tip 1. Compare policies wisely by gathering multiple quotes. Focus on both premiums and key features like coverage options, exclusions, customer support, and claim procedures, to find the best fit for your needs.

Get your hands on two to three quotes and compare them not just based on premium, but also look for attributes like policy inclusions & exclusions, customer support service, online reviews, claim process, and repair shop network.

Tip 2. When in doubt, ask questions

It is essential to get clarity when it comes to insurance. Don’t know what questions to ask -

- What documents are required to file a claim?

- What situations are excluded from coverage?

- How long does the claim process take?

- Are flood damages covered in the policy?

- Are car modifications covered?

Note that the more informed you are, the less surprised you’ll be during crises.

Also Read: Is SRCC add-on car insurance worth it for Filipino car owners in 2026?

How to file a total loss claim successfully

If your vehicle has been declared a total loss, follow these steps carefully.

Collect the following documents

- Insurance policy papers

- Vehicle’s Official receipt and Certificate of Registration

- Driver’s license

- Police report

- Photos of damage and the incident scene

- Duly filled claim forms

Note that it is always a good idea to be extra prepared. So, get digital and physical copies whenever possible.

What not to do when filing claims

- Make sure to avoid these common errors:

- Delaying reporting the incident to the provider

- Giving out misleading information about the event

- Submitting incomplete documents

- Repairing without insurer approval or at an authorised repair shop

- Not disclosing modifications

Remember, honesty and accuracy improve your chances of claim approval.

Also Read: Got a new high-end car? Here is the best insurance guide (for 2026)

Bottom line

Misconceptions about car insurance can lead to costly mistakes, especially when dealing with a situation as serious as a vehicle’s total loss. It is therefore important to have a clear understanding of total loss coverage to make smarter decisions, avoid denied claims, and protect your finances more effectively.

The best approach is quite simple: read the policy fine print, do not shy away from asking questions, compare at least 2 to 3 providers, and never rely solely on online advice.

Remember, car insurance isn’t just a formality; it’s a financial protection plan that could save you from unexpected situations while you are on the go.

Also Read: Fake car insurance: How to verify your provider

FAQs

Q1. When does a vehicle qualify as a total loss?

Ans. A vehicle is considered a total loss by the provider when its repair costs exceed its market value or reach the insurer’s repair threshold.

Q2. Is flood coverage included in a standard car insurance policy?

Ans. No. Flood coverage usually requires an additional Acts /of Nature add-on in the policy.

Q3. Can I negotiate my total loss payout with the insurer?

Ans. Yes, absolutely. However, you can put supporting documents and comparable market values on the negotiation table.

Q4. How long does a total loss claim usually take?

Ans. Processing times vary from one to several weeks, depending on the completion & accuracy of the documents and investigation requirements.

Q5. Are second-hand cars considered for total loss coverage?

Ans. Yes, many insurers cover second-hand vehicles, but they need to meet inspection requirements.

Q6. Will my insurer pay for aftermarket accessories in the payout for total-loss coverage?

Ans. Only if those accessories were declared and the payout was included in your policy.

Q7. Will my claim get denied because of drunk driving?

Ans. Yes, without a doubt. You see, driving under the influence is commonly excluded from coverage.

Q8. Is theft considered total loss?

Ans. In many cases, yes, especially if the vehicle is unrecovered or heavily damaged after recovery.

Q9. Is it worth getting Acts of Nature coverage?

Ans. Absolutely. Due to the frequent typhoons and flooding, this coverage is highly recommended for Filipino drivers.

Also Read: Smart insurance tips for Ducati, BMW, and Harley-Davidson owners