Who doesn't love a good adventure trip? Whether it’s a spontaneous weekend getaway or a months-long bucket-list family trip, travelling is a great way to rejuvenate and spend quality time with friends and family. To make the most out of our trip, we spend weeks planning our itineraries, hunting for cheap airline tickets, and curating the perfect outfits for the ‘gram.

But there is one boring detail that most of us leave until the very last minute: travel insurance.

Let’s be completely honest: no one gets excited about reading insurance policies. It feels like an extra expense, an annoying add-on that takes away from our pocket money for souvenirs and local street food. It is incredibly tempting just to tick the "No, thank you" box when booking a flight and hope for the best.

But relying solely on luck can ruin a vacation faster than a sudden typhoon. If you have ever been stuck at the airport for nine hours because of a delayed flight, or had your luggage vanish into thin air, you already know that travel can be deeply unpredictable.

So, how do you navigate this? Do you need insurance when you’re just visiting your grandma in Davao? Do you need a separate one when crossing borders? Do you actually need both? Let’s break it down once and for all.

Also Read: What is travel insurance, and why every Filipino traveller should understand it

The local getaway (Domestic travel insurance)

Let’s start close to home. You’re packing your bags for a quick flight to Boracay, Palawan, or Cebu. You’re still in the Philippines, you speak the language, and you know how to navigate the local system. Do you really need to buy travel insurance for a domestic trip?

To answer that, we have to look at what domestic travel insurance actually does.

What does domestic travel insurance cover?

AI-Generated Image

AI-Generated ImageDomestic travel insurance is specifically designed for trips within the Philippines. As you aren’t leaving the country, it doesn’t focus on the costs of massive medical bills. Instead, it serves as a financial cushion in the event of a logistics mishap. It typically covers:

- Trip cancellations and delays: If a sudden typhoon rolls in and cancels your flight to Coron, your insurance can help reimburse you for non-refundable hotel bookings. If you are stuck at the airport for hours, it can cover your meal costs.

- Baggage loss or damage: If the airline accidentally sends your suitcase to one place while you are landing at another location, your travel insurance policy will give you a cash allowance to buy emergency clothes and toiletries.

- Emergency medical expenses: If you get a nasty stomach ache or food poisoning from eating seafood or get hurt while island-hopping, it covers immediate medical treatment while you are away from your home city.

- Accidental death and disability: This one’s the bad part no one wants to talk about, but it’s there to protect your family just in case the absolute worst happens.

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

The "but I have an HMO!" argument

This is the number one reason Filipinos skip domestic travel insurance. You might think, "My company gave me a Maxicare/Medicard, and I pay my PhilHealth contributions regularly. Why do I need more insurance?"

It is a valid point, but here is the catch: your HMO only cares about your health. It does not care about your vacation.

If you get sick in Cebu, yes, your HMO will likely cover your hospital room. But if the airline loses your laptop, or your flight is delayed by 12 hours, your HMO will not give you a single peso.

Furthermore, many local HMOs have limited networks in remote provinces. If you are on a remote island, the nearest clinic might not accept your specific health card, forcing you to pay cash up front.

Domestic travel insurance is incredibly cheap (around PHP 200 to PHP 500 depending on the duration). It fills the massive gaps left by your regular health card.

Crossing borders (International travel insurance)

Now, let’s talk about stepping onto an international flight. The moment you clear immigration at NAIA and board a plane taking you to another country, the stakes get significantly higher.

Why international insurance is a different game altogether

When you are in a foreign country, you lose your home-court advantage. You don’t know how the local hospitals work, you might not speak the language, and most importantly, your local Philippine HMO and PhilHealth are mostly useless. For instance, if you land in a hospital in Singapore, Tokyo, or New York, you are entirely on your own.

International travel insurance is heavily focused on emergency medical assistance. This means if you get critically ill or severely injured in a place without proper medical facilities, the insurance company will pay the staggering cost of flying you out on a medical helicopter or plane to the nearest proper hospital, or flying you back home to the Philippines.

Without insurance, a medical evacuation can easily cost millions of pesos, a financial burden that can bankrupt an average Filipino family.

AI-Generated Image

AI-Generated ImageBeyond medical assistance: The travel inconveniences

Aside from saving you from the massive hospital bills, international insurance handles the nightmares of global transit:

- Lost passport assistance: Losing your passport in a foreign country is an absolute nightmare. A good international policy will help cover the costs of obtaining emergency travel documents from the Philippine embassy. It will even reimburse you for the extra hotel nights you had to spend waiting for them.

- Trip interruption: If an emergency arises back home, such as a family member being critically ill, you may cut your vacation short and fly back immediately. International insurance usually covers the cost of your last-minute, expensive return flight.

Also Read: The most common travel insurance myths Filipinos still believe

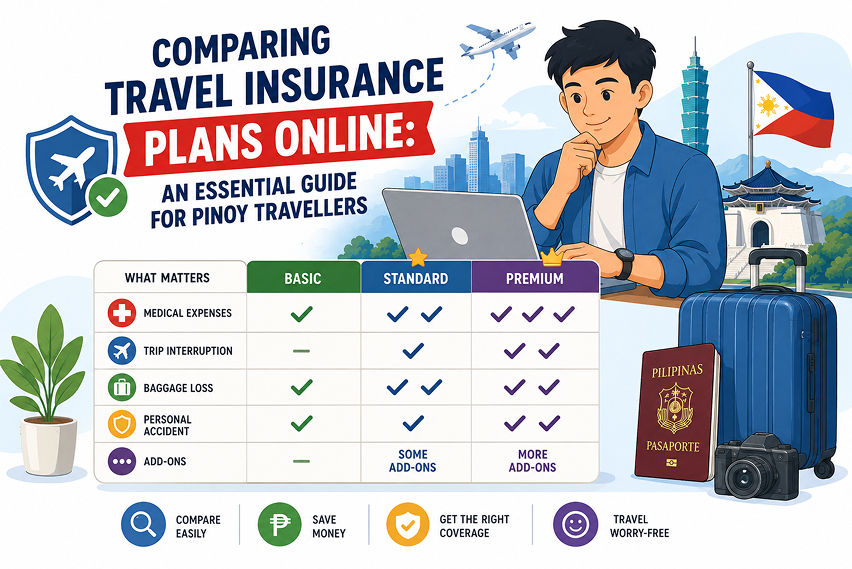

Domestic vs. International travel insurance

To make it crystal clear, let’s put them side by side. You don't need to buy both at the same time for the same trip, but you need to understand which tool to use for which scenario.

|

Feature |

Domestic Travel Insurance |

International Travel Insurance |

|

Geographic Scope |

Within the Philippines only |

Outside the Philippines |

|

Medical Coverage Limits |

Relatively low |

Very high |

|

HMO/PhilHealth Integration |

Works alongside your local health coverage |

Replaces your local coverage |

|

Key Focus |

Flight delays, cancellations, lost luggage |

Massive medical emergencies, evacuation, and lost documents |

|

Average Cost |

Very cheap |

Moderate (depending on the country) |

The Golden Rule: Match the policy to the border

Can you use an international policy for a domestic trip? No.

Can you use a domestic policy for an international trip? Absolutely not.

They are two separate products designed for entirely different risks. If you are travelling frequently, say, doing three local trips and two international trips a year, we’d suggest considering an annual travel insurance plan. Why? This covers you for an unlimited number of trips within 365 days, saving you the hassle of buying a new plan every single time you pack a bag.

Bottom line

At the end of the day, skipping travel insurance might save you a few hundred pesos. But it can also cost you thousands later. When buying travel insurance, the decision between domestic and international coverage depends on your destination. For local trips, domestic coverage gives you peace of mind at a low cost, even amid chaotic flight schedules and lost baggage. For international trips, comprehensive insurance is your shield against catastrophic medical bills abroad.

We suggest treating insurance as a non-negotiable part of your travel budget, packing your bags, and enjoying your trip without any ‘what if’ thoughts.

Also Read: Smart travel: Should you buy travel insurance for one trip or the whole year?

FAQs

Q1. Is travel insurance strictly mandatory for Filipinos leaving the country?

Ans. It depends entirely on where your passport is taking you.

- Mandatory: If you are applying for a visa to the Schengen Area (Europe), you are legally required to present a travel insurance policy with a minimum medical coverage. No insurance, no visa. Countries like Cuba and Qatar also strictly require it upon entry.

- Highly recommended/optional: For visa-free Asian destinations like Thailand, Singapore, or Hong Kong, it is generally not legally mandated.

Q2. Can I just rely on the free insurance from my credit card?

Ans. Many premium credit cards advertise "Free Travel Insurance" if you use their card to purchase your plane tickets. While this is a fantastic perk, you must read the fine print.

Often, these complementary policies are very basic. They might cover accidental death or severe flight delays, but offer very little or zero coverage for standard medical illnesses.

Q3. Will insurance cover me if a typhoon cancels my flight?

Ans. Yes, but timing is everything. Insurance is designed to cover unforeseen events.

- If you buy your travel insurance two weeks before your trip, and a sudden typhoon forces the airline to cancel your flight, your insurance will cover your losses.

- If a typhoon is already spinning inside the Philippine Area of Responsibility (PAR) and authorities have issued warnings, and then you rush to buy insurance online because you are scared of a cancellation, the insurance company will reject your claim.

Q4. What is a "pre-existing medical condition", and should I care?

Ans. This is the number one reason insurance claims get denied, and it angers up a lot of travellers. A pre-existing condition is a health concern that you already have before buying the policy, like asthma, diabetes, high blood pressure, or heart problems. Most standard, cheap travel insurance policies do not cover pre-existing conditions. If you have a known medical condition, it is recommended to choose a policy that explicitly covers pre-existing conditions.

Q5. Do I really need domestic travel insurance if I already have PhilHealth and an HMO?

Ans. It is easy to think you are fully covered at home because you have a local health card (HMO) or PhilHealth. But your HMO won't do anything if the airline loses your suitcase, or if a typhoon cancels your flight, and you lose all the money you spent on a non-refundable hotel. Domestic travel insurance is quite cheap, and it covers those annoying travel headaches that your regular health insurance simply ignores.

Q6. From where can I buy travel insurance?

Ans. It has never been easier to buy insurance. You can get it directly when booking your flights, or you can also buy comprehensive plans online within minutes from reputable local and international providers.