No matter how meticulously you map out your itinerary, pack your bags, or lock in early-bird discounts, travel always retains an element of unpredictability. A sudden weather shift can ground your flight, a local dish might not sit well with your stomach, or your suitcase could end up on a completely different continent.

While it's easy to view travel insurance as merely another checkbox on your pre-trip to-do list, having the right policy functions as a financial and emotional safety shield. It can transform a catastrophic vacation into a manageable, minor detour.

Also Read: Falling ill while travelling? Here's how travel insurance will come to your rescue

Understanding the four pillars of travel insurance protection

Not all insurance policies are built the same way. To find a plan that fits your specific travel style, start by understanding the four primary pillars that safeguard your journey:

Emergency medical care & evacuation: This is arguably the most critical component. If you fall severely ill or sustain a major injury abroad, local healthcare costs can skyrocket. Medical protection ensures your hospital stays, physician consultations, and, in severe cases, even emergency medical airlifts or repatriation are managed without draining your bank account.

Trip disruption & cancellations: Life happens. If an unexpected event forces you to cancel or cut your trip short, such as an urgent medical emergency or a sudden job loss, travel insurance helps reimburse your non-refundable expenses, including flights, hotel bookings, and tour deposits.

AI-Generated Image

AI-Generated ImageLuggage and personal effects: When an airline misplaces your bags or your digital camera is stolen from a crowded tourist spot, baggage protection steps in. It provides compensation to replace the items you lost (up to the policy limits) or offers a monetary buffer to purchase essentials while your delayed bags are being tracked down.

Transit and travel delays: If a severe storm or a technical glitch leaves you stranded at the airport, travel insurance covers the financial fallout. How? It reimburses out-of-pocket expenses for meals, ground transportation, and overnight hotel stays incurred during the delay.

Also Read: Smart travel: Should you buy travel insurance for one trip or the whole year?

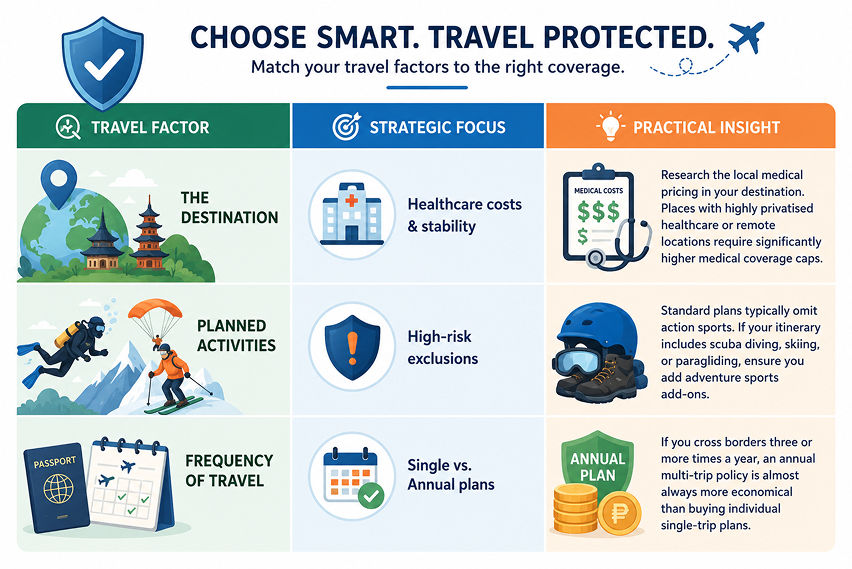

How to tailor coverage to your specific journey

Finding the ideal policy requires looking at the unique variables of your upcoming trip. A weekend city break requires a completely different approach than a month-long mountain expedition.

AI-Generated Image

AI-Generated ImageAlso Read: Traveller's blueprint: How and when travel insurance pays for emergencies

Pitfalls to sidestep: Decoding the fine print

To avoid surprises when you attempt to file a claim, it is essential to look past the marketing headlines and analyse the precise terms of your contract:

Understand your deductibles: What is a deductible? It is the amount the insured pays before the insurance provider covers the remaining amount. While a plan with a higher deductible usually means a cheaper upfront premium, make sure it’s an amount you can easily afford in an emergency. Note: Not all travel insurance policies include a deductible.

Check the caps: Every policy has maximum payout limits for different categories. Ensure the maximum medical limit is sufficient for your destination, and check whether the baggage limit covers high-value items like laptops or smartphones.

Know the exclusions: No travel insurance policy covers everything. Standard exclusions usually include extreme sports and incidents arising from pre-existing medical conditions. Knowing the boundaries beforehand keeps you prepared and protected.

Modern insurance solutions: Digital protection

Securing reliable protection no longer requires long, in-person appointments or managing piles of confusing paperwork. Modern insurance providers have reimagined the experience to fit directly into a digital lifestyle.

For travellers seeking seamless, budget-friendly options, there are excellent options making coverage accessible. With plan options starting at PHP 299, travel insurance can comfortably fit into any travel budget.

Nowadays, the entire process is optimised for speed: you can input your trip details online, generate a real-time customised quotation, and complete your purchase in minutes. Also, the platforms are designed to offer instant online issuance; your coverage activates immediately upon purchase. Further, most providers back their plans with a 24/7 emergency support team, ensuring that, no matter what time zone you're in, a helping hand is always just a quick phone call away.

Also Read: Travelling with kids? Don't skip these travel insurance tips

Bottom line

Ultimately, investing in travel insurance is about protecting your experiences and your finances. All you need to do is take a few moments to evaluate your itinerary, select a responsive & modern provider, and decode the insurance policy guidelines. This will grant you the ultimate travel luxury, the freedom to explore the world in full peace.

With travel insurance by your side, you can focus entirely on making unforgettable memories, knowing you are prepared for all the twists and turns the journey brings.

Also Read: Maximising your peace of mind: Traveller's guide to Hong Kong travel insurance

FAQs

Q1. Do travel insurance policies cover pre-existing health conditions automatically?

Ans. No. Standard travel insurance plans usually exclude pre-existing medical conditions. However, some providers offer specialised waivers or premium add-ons that can extend coverage to these conditions.

Q2. What benefits should you look for in an insurance provider?

Ans. Go for a provider that focuses on speed, affordability, and accessibility. In addition, it always helps to have access to real-time digital quoting, instant policy issuance directly online, and round-the-clock 24/7 customer assistance during emergencies.

Q3. Is it worth getting a travel insurance policy for domestic trips?

Ans. Yes, getting a domestic travel insurance policy can be super beneficial. It offers coverage for non-refundable flight cancellations, lost or damaged luggage, and prolonged transit delays within your home country.

Q4. Which documents must I keep handy while travelling?

Ans. Always keep a digital and a physical copy of your insurance policy certificate, as well as the provider's emergency 24/7 contact phone numbers. If you need to make a claim, remember to save all official receipts, medical reports, police statements, or airline delay certificates.

Q5. Can I purchase a policy after I have already started my trip?

Ans. Most insurance companies require you to buy your policy before your official departure date. Purchasing a plan after leaving your home country can significantly limit your insurance coverage options.

Q6. How can I find the best balance between my insurance policy's price and coverage?

Ans. Avoid selecting a policy solely because of its low price. Instead, look at the value it offers. Start by comparing the policy limits to the actual cost of medical care at your destination, reviewing the exclusions, and ensuring the deductibles match your financial comfort level.

Also Read: The ultimate guide to buying travel insurance online: What every Filipino traveller needs to know