Welcome back to the final part of our ultimate travel insurance breakdown! If you read Part 1 and Part 2, you are already way ahead of most travellers when it comes to safety during vacations or work trips. We have already discussed flight delays, medical emergencies, and what to do if a pickpocket steals your passport.

But wait, there is even more! Inside an insurance policy document, some final, very important words act like the "secret ground rules" of the whole deal between you & your insurer. These are the terms that tell you exactly how the insurance company calculates your money and what types of emergencies count as true accidents.

Also Read: Smart travel: Should you buy travel insurance for one trip or the whole year?

Let's dive into Part 3 of our guide to travel insurance policy terms. As always, we will keep it super easy to understand so you can be a complete travel master!

1. Safety first: Words about your body and accidents

When we travel, we hope everything goes smoothly, so we get insurance. And do you know that policies have a section dedicated to serious accidents? Here are the terms they use to explain how they protect your body.

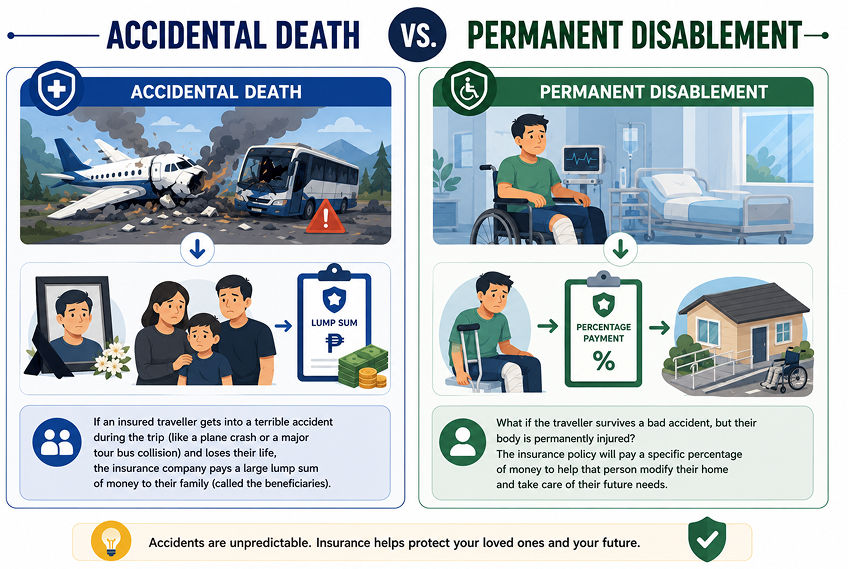

Accidental death vs. Permanent disablement

These are heavy words, but they are very important for a traveller's financial safety net.

- Accidental death: If an insured traveller gets into a terrible accident during the trip (like a plane crash or a major tour bus collision) and loses their life, the insurance company pays a large lump sum of money to their family (called the beneficiaries).

AI-Generated Image

AI-Generated Image- Permanent disablement: What if the traveller survives a bad accident, but their body is permanently injured? For example, if they lose their eyesight or can no longer use their hands or legs for the rest of their life. The insurance policy will pay a specific percentage of money to help that person modify their home and take care of their future needs.

Also Read: Domestic vs. International Travel Insurance: A complete guide for Filipino travelers

Bodily injury

In the insurance world, bodily injury has a very specific meaning. It means physical harm or damage caused entirely by an external, violent, accidental, and visible event. For example, if you slip on a wet floor at the airport and break your arm, that is a bodily injury. But if you wake up with a normal headache or a stomachache, that is considered an illness, not a bodily injury.

2. Counting the money: How benefits are paid out

Have you ever wondered how an insurance company decides exactly how many pesos to give you when things go wrong? They use these terms to explain the math.

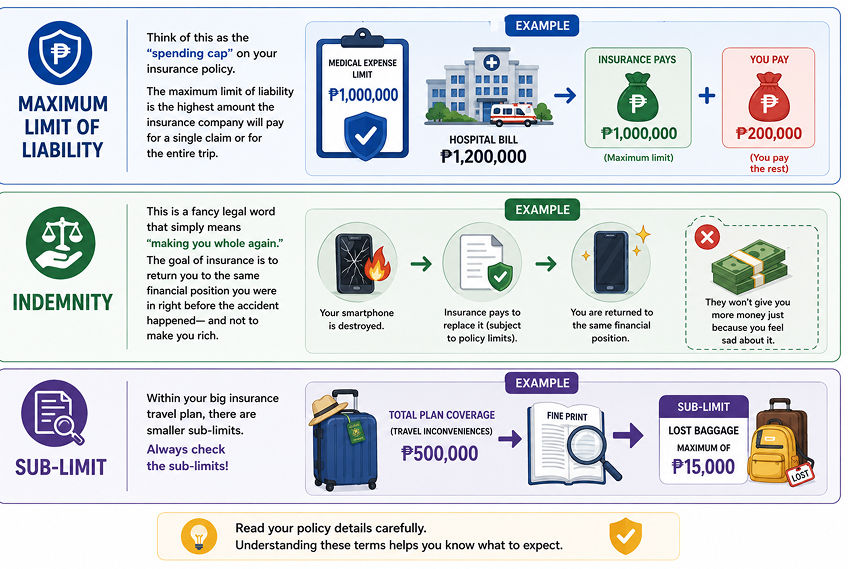

Maximum limit of liability

Think of this as the "spending cap" on your insurance policy. The maximum limit of liability is the highest amount the insurance company will pay for a single claim or for the entire trip. For example, if your plan sets the limit for medical expenses at PHP 1,000,000, and your hospital bill in another country reaches PHP 1,200,000, the insurance will pay the maximum of PHP 1,000,000, and you will have to pay the remaining PHP 200,000 yourself.

Indemnity

This is a fancy legal word that simply means "making you whole again." The goal of insurance is to return you to the same financial position you were in right before the accident happened— and not to make you rich. If your PHP 10,000 smartphone is destroyed in a luggage fire, the insurance company will pay to replace it (subject to policy limits). They won't give you PHP 100,000 just because you feel sad about it.

AI-Generated Image

AI-Generated ImageSub-limit

Do you know that within your big insurance travel plan, there are smaller sub-limits? So, imagine your total plan covers up to PHP 500,000 for travel inconveniences, but inside the fine print, there might be a sub-limit that says, "Maximum of PHP 15,000 for lost baggage." Meaning, even though your total plan is huge, you can only get up to PHP 15,000 for that specific bag problem. Always check the sub-limits!

Also Read: The most common travel insurance myths Filipinos still believe

3. The rules of the game: Legal terms made simple

Before the insurance company issues a check, they verify that everyone has complied with the contract's official rules.

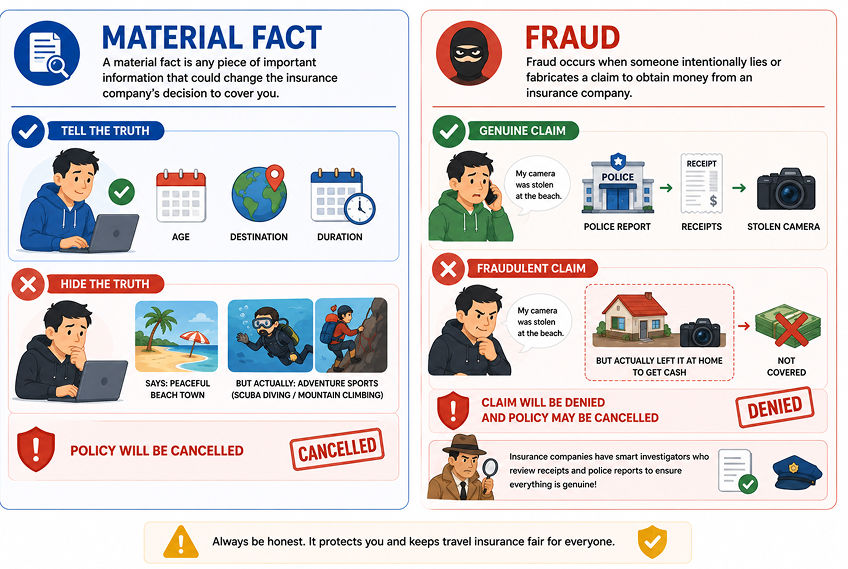

Material fact

A material fact is any piece of important information that could change the insurance company’s decision to cover you. For example, when you apply for insurance, you must tell the truth about your age, where you are travelling, and how long you will be gone. If you lie and say you are travelling to a peaceful beach town, but you are actually flying out to participate in adventure sports like scuba diving or mountain climbing, you have hidden a material fact, and your policy will be cancelled.

AI-Generated Image

AI-Generated ImageFraud

This is a word we hear in detective movies, but it applies to travel insurance, too. Fraud occurs when someone intentionally lies or fabricates a claim to obtain money from an insurance company. For example, if a traveller claims their expensive camera was stolen at the beach, but they actually left it at home in the Philippines on purpose to get cash, that is fraud. Insurance companies have smart investigators who review receipts and police reports to ensure everything is genuine!

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

Final thoughts: You are now an insurance expert!

You did it! You have officially c

onquered all three parts of our travel insurance vocabulary guide by ZenInsure. By taking the time to understand these travel insurance policy terms, you are no longer clicking "agree" unquestioningly. Now you know your rights, your limits, and you know exactly how to protect your family and your hard-earned savings.

As you pack your bags, download your digital insurance policy, keep the emergency hotline number on your phone, and head out to explore the world with absolute confidence.

Also Read: What’s not covered under a travel insurance policy? A must-read for Filipino travellers

FAQs

Q1. What happens if my total medical bill is more than the maximum limit of liability?

Ans. If your medical bills go over the maximum limit stated in your policy schedule, the insurance company will only pay up to that exact cap. You or your family will be responsible for paying the remaining balance out of pocket. That is why it is always smart to choose a plan with a higher limit when travelling to countries with very expensive healthcare, like the USA or Europe.

Q2. What is the difference between an illness and a bodily injury in a policy?

Ans. A bodily injury is caused by something sudden and violent outside your body, like falling down the stairs or getting hit by a surfboard. An illness is a sickness that starts inside your body, such as catching the flu, getting food poisoning, or developing a sudden fever. Most policies cover both, but under different sections with different rules!

Q3. What happens if I accidentally forget to mention a minor pre-existing health issue?

Ans. If you forgot to mention a minor check-up from a year ago, it might still affect your claim if that specific health issue causes an emergency during your trip. If the insurance company learns it was a known medical condition during their routine check, they can deny the medical claim under the pre-existing condition rule.

Q4. If my bag is stolen, does the insurance company give me cash to buy a brand-new version of everything I lost?

Ans. Because of the rule of Indemnity, insurance companies usually calculate the "actual cash value" or depreciation of your items. This means they look at how old your clothes and bags were and pay you what they were worth right before they were stolen, rather than the price of brand-new items.

Q5. Who receives the money if an "accidental death" claim is paid out?

Ans. The money is paid directly to your designated beneficiary. When you fill out your travel insurance application form, there is a section where you name a trusted person (like a parent, sibling, or spouse) to receive the benefit if a worst-case scenario happens.

Also Read: A complete guide to travel insurance for different travellers