Imagine a day when you have your bags packed, your itinerary ready, and your camera is fully charged. You have landed at your dream destination and are all set to enjoy the street food, the local market, and all the hidden spots you saved on Instagram. But suddenly, something doesn’t feel right, your stomach starts to hurt, or worse, you trip and twist your ankle.

Getting sick or hurt while vacationing in another country is a scary thought for anyone. Away from home, you need to visit hospitals where people do not speak your language, and bills can drain your bank account.

Don’t worry, this guide will teach you exactly how to protect yourself, how travel insurance keeps you safe, and what to do if you need a doctor while exploring the world.

Also Read: What is travel insurance, and why every Filipino traveller should understand it

Why getting sick overseas is a financial trap for Filipinos

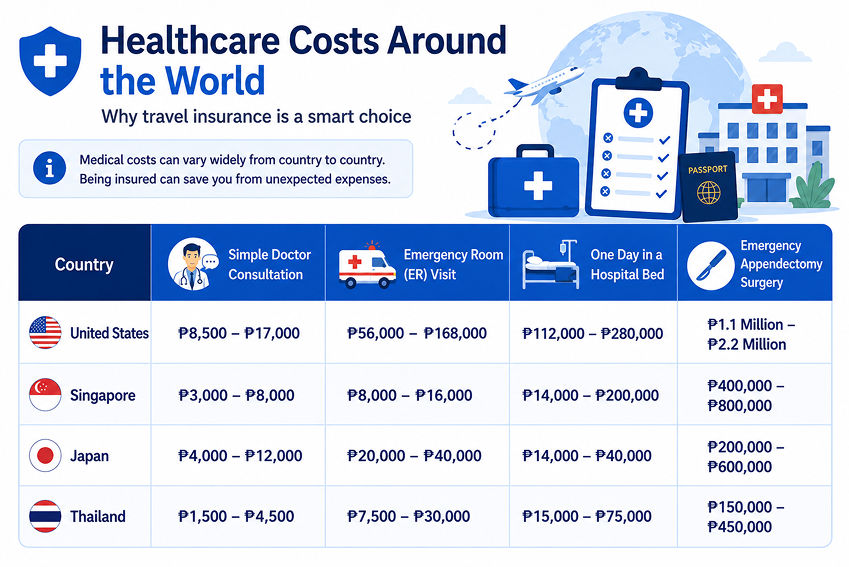

We Pinoys love to save money by looking for cheap flights and budget hotels. However, we often forget about the massive cost of healthcare in other countries. In the Philippines, we might complain about hospital bills, but overseas, those costs can swell up to a hard-to-digest number.

The cold truth about local coverage

One of the most common mistakes Filipino travellers make is assuming their regular health shields will protect them across borders.

- PhilHealth limitations: PhilHealth is designed for use within the Philippines. Under current regulations, it offers very limited financial support for medical bills incurred abroad, and the process to claim a small reimbursement after you return is long and tedious. It will never pay a foreign hospital directly.

- HMO restrictions: Your company or personal Health Maintenance Organisation (HMO) plan usually stops working the moment your plane leaves Manila. Very few premium HMOs cover international emergencies, and even then, they only offer low reimbursement limits.

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

A look at real-world foreign medical costs

AI-Generated Image

AI-Generated ImageIf you do not have a specialised travel insurance policy, you will have to pay the bill upfront at foreign hospitals. If you aren’t able to provide a credit card or cash immediately, some facilities may even delay your treatment, turning a manageable illness into a life-threatening crisis.

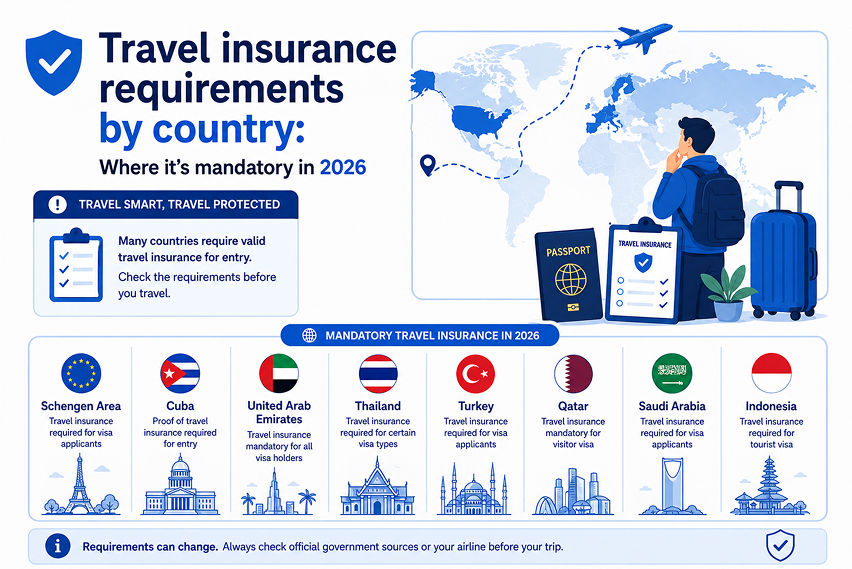

Also Read: Travel insurance requirements by country: Where it's mandatory in 2026

The hidden safeguards: Crucial travel insurance benefits

A basic travel insurance policy bought in the Philippines does much more than just look after your lost luggage. Under the Insurance Commission of the Philippines' rules, a comprehensive travel plan must include several lifesaving medical triggers.

1. Emergency medical evacuation

If you are hiking in a remote village in Vietnam or exploring an island in Indonesia and suffer a severe injury, the local clinic might not have the tools to save you. This benefit pays for a helicopter, ambulance, or specialised plane to fly you to the nearest high-quality hospital, or, if needed, even back to a medical centre in Manila. Without insurance, a medical flight can easily cost you over a million.

2. Repatriation of remains

It is a sad topic, but an important one. If a Filipino passes away while travelling abroad, the legal and logistical costs to bring their body back home to their family can break a household financially. Insurance covers these massive expenses and handles the complex international paperwork.

3. Direct hospital billing and 24/7 hotlines

Good travel insurance providers give you a phone number you can call anytime, day or night. If you are admitted to a hospital, the insurance company can issue a statement to the foreign hospital saying that it will pay the bills directly, meaning you do not have to swipe your own credit card for millions of pesos.

Also Read: What does travel insurance actually cover in the Philippines?

Step-by-Step: What to do if you fall ill abroad

If you wake up with a terrible fever or break a bone during your trip, do not panic. Follow this step-by-step guide to ensure your health is managed and your insurance claim stays valid.

1. Call your insurance hotline first: Do this immediately

Before you check into a hospital (unless it is a life-or-death emergency), call the 24/7 emergency number listed on your travel insurance policy. The agents will tell you exactly which nearby hospitals accept their direct billing, so you do not have to pay cash.

2. Present your policy and passport

At the hospital admissions desk, present your travel insurance certificate and Philippine passport. Keep a digital copy of your policy on your smartphone so you can email it to the authorities when asked without delay.

3. Gather every piece of paperwork

Before checking out, make sure you have acquired all the bills, receipts, and other documents. For instance, if you have made small out-of-pocket expenses for pharmacy medicines or a quick clinic checkup, collect all official receipts, detailed medical reports, doctor prescriptions, and laboratory results. These original documents are required for processing reimbursements back in the Philippines.

4. File your claim within the deadline

Upon returning to the Philippines, most insurance companies would require you to submit your formal claim as soon as possible. Make sure to complete the claim forms and attach all the paperwork you gathered abroad.

Also Read: The most common travel insurance myths Filipinos still believe

Common sickness traps and legal rules to watch out for

Navigating travel insurance rules can be tricky. To ensure your claims are not rejected, you must understand three critical legal concepts used by insurers.

AI-Generated Image

AI-Generated ImageThe pre-existing condition trap

Let us say you have asthma, diabetes, or a heart condition that you treat regularly at home in the Philippines. If you travel abroad and have a sudden asthma attack because of cold weather, a standard travel insurance policy will not cover your hospital bills.

Insurance rules define a pre-existing condition as any illness you already had or received treatment for before buying the policy. If you have a chronic illness, you must look for an advanced travel policy that explicitly includes this add-on coverage.

Alcohol, extreme sports, and negligence

Insurance will not protect you if your actions violate the law or general safety guidelines.

The drinking exclusion: If you get into a street accident in Thailand after drinking several bottles of alcohol, the insurer will check your medical reports. If alcohol were in your system, they have the legal right to deny your claim entirely.

Adventure activities: Standard policies do not cover injuries from "hazardous sports" like scuba diving without a license, skydiving, or riding an unregistered scooter without a helmet. Always read the fine print before trying high-risk activities.

Also Read: Domestic vs. International Travel Insurance: A complete guide for Filipino travelers

The Schengen visa requirement

If you are planning a trip to Europe, travel insurance is not optional. Rather, it is a strict legal requirement. To get a Schengen Visa, Filipinos must show proof of travel insurance that provides a certain minimum amount of emergency medical coverage and includes repatriation benefits.

Also Read: Smart travel: Should you buy travel insurance for one trip or the whole year?

Wrapping Up

You see, at the end of the day, travelling is all about making beautiful memories with friends and family. You get to try delicious foods, experience new cultures, and whatnot. While planning all this, it is also crucial to invest a few thousand pesos towards a reliable travel insurance policy. This would ensure that a trip to a foreign emergency room remains a minor bump in the road rather than a financial disaster that ruins your trip and savings.

So, pack your bags, secure your policy, and explore the world with a peaceful mind.

Also Read: Traveller's blueprint: How and when travel insurance pays for emergencies

FAQs

Q1. Can I buy travel insurance if I am already outside the Philippines?

Ans. No. You must purchase your travel insurance policy before your flight leaves the Philippines. If you try to buy a policy while already walking around another country, the policy will be considered invalid, and any claims you make will be denied.

Q2. What should I do if the foreign hospital does not speak English?

Ans. If you are facing a tough language barrier, call your insurance provider's 24/7 emergency hotline immediately. Most international insurance travel assistants provide translation services. They can speak directly with the foreign doctors to understand your diagnosis and arrange your care.

Q3. Does travel insurance cover my regular maintenance medicines?

Ans. No. Travel insurance is strictly for sudden, unexpected medical emergencies. It does not cover the cost of buying your daily maintenance medicines for chronic issues like high blood pressure or diabetes. It is suggested to always pack more than enough of your prescribed medications in your carry-on luggage before leaving.

Q4. What happens if my flight home is delayed because I am stuck in a foreign hospital?

Ans. If a doctor officially states that you are too sick to fly, a good travel insurance policy will automatically extend its coverage days for free. Many plans will also help cover the cost of changing your airline ticket and pay for extra hotel nights for a family member staying behind to watch over you.

Q5. Does travel insurance cover motorcycle or scooter accidents?

Ans. They are only covered if you follow strict legal rules. To get coverage, you must hold a valid driver's license that is recognised in that country (or an International Driving Permit), you must be wearing a proper safety helmet, and you cannot be under the influence of any alcohol or illegal substances.

Q6. How long does it take to get my money back for a reimbursement claim?

Ans. According to general guidelines from the Insurance Commission, once all correct documents and receipts are submitted, standard claims are usually processed and paid out within 20 to 30 business days.