We all love going on vacations, right? But let’s be honest for a second. While it is fun planning itineraries, nobody likes thinking about what could go wrong. Flights get delayed, bags mysteriously disappear in transit, or worse, someone in the group catches a bad stomach flu after trying exotic street food.

This is exactly where travel insurance comes into play.

Many Filipinos treat travel insurance like a checkbox on their visa application. It is something many travellers buy because the embassy requires it, or it is a small add-on you don’t mind clicking while booking a flight online. But when a real emergency strikes, having a policy brings significant relief. But here's a catch: only having insurance isn’t enough; you actually need to understand what it says.

Reading an insurance policy can feel like trying to decode ancient text. It is filled with dense legal jargon that can make your head spin. To help you protect your hard-earned money, we have broken down the travel insurance policy terms every Filipino traveller needs to understand before booking their next adventure.

Also Read: What does travel insurance actually cover in the Philippines?

Why understanding insurance jargon matters

Before we dive into the specific vocabulary, let’s talk about why this matters. Imagine arriving in Seoul during winter, only to find out your suitcase didn't make the flight. You're freezing, you have no change of clothes, and you need to buy a heavy jacket immediately.

You call your insurance provider, confident they will cover the cost, only to hear: "Sorry, but according to your policy's definitions, this specific scenario isn't covered." Ouch.

Knowing your travel insurance policy terms keeps you from experiencing heartbreak at the claims counter. It helps you know exactly what you are paying for, how to file a claim correctly, and how to avoid getting your claim denied. Let’s look at the most common terms you will encounter in standard Philippine travel insurance policies.

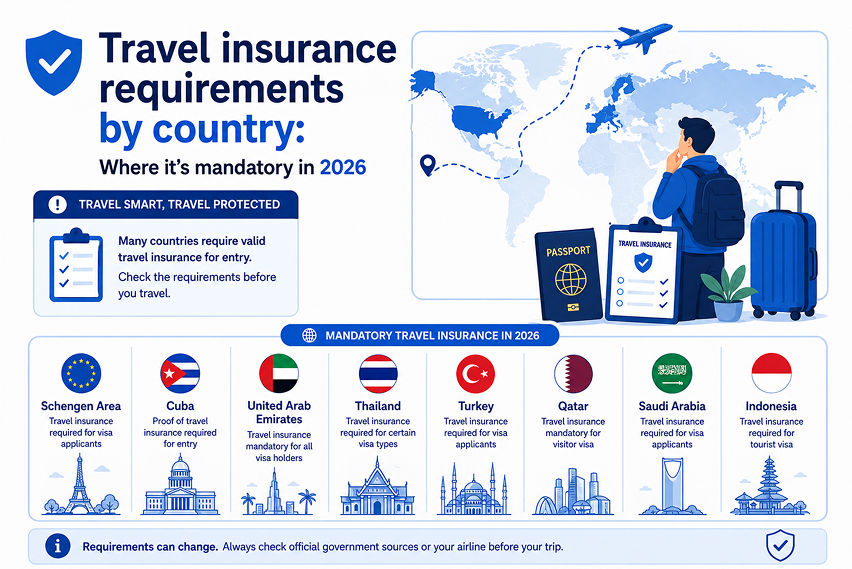

Also Read: Travel insurance requirements by country: Where it's mandatory in 2026

1. The core terms: Who, when, and where?

Let’s start with the absolute basics. These terms set the boundaries of your coverage. If you get these wrong, your entire policy might become useless.

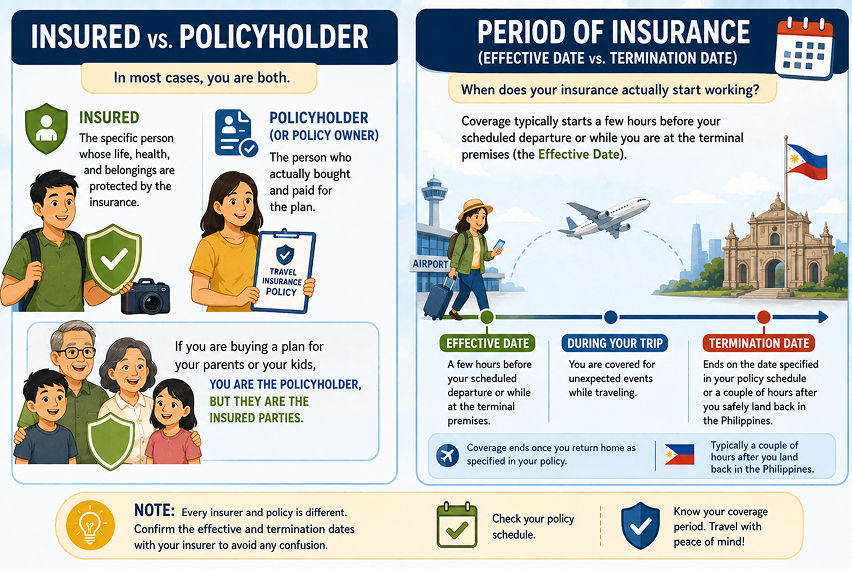

Insured vs. Policyholder

In most cases, you are both. The Insured is the specific person whose life, health, and belongings are protected by the insurance. The Policyholder (or policy owner) is the person who actually bought and paid for the plan. If you are buying a plan for your parents or your kids, you are the policyholder, but they are the insured parties.

AI-Generated Image

AI-Generated ImagePeriod of insurance (Effective Date vs. Termination Date)

When does your insurance actually start working? Many Filipinos believe that coverage only begins the moment their feet touch foreign soil.

In reality, for most plans, coverage typically starts a few hours before your scheduled departure or while you are at the terminal premises (the Effective Date). It officially ends either on the date specified in your policy schedule or a couple of hours after you safely land back in the Philippines (the Termination Date).

Note, every insurer and policy is different. It is therefore a good idea to confirm the effective and termination dates with your insurer to avoid any confusion.

Usual country of residence

For local insurance policies bought in Manila, Cebu, or anywhere else in the country, the Usual Country of Residence must be the Republic of the Philippines. This means the trip must officially start and end here. You cannot fly to Singapore, realise you forgot to buy insurance, buy a Philippine policy while sitting in a cafe, and expect it to be valid. You must be physically present in the Philippines when purchasing it before your trip begins.

Also Read: Traveller's blueprint: How and when travel insurance pays for emergencies

2. Medical Emergencies: Reading the fine print

Getting sick abroad is scary and incredibly expensive. A short hospital stay in places like the USA, Singapore, or Japan can easily cost hundreds of thousands of pesos. Here are the medical travel insurance policy terms you must watch out for.

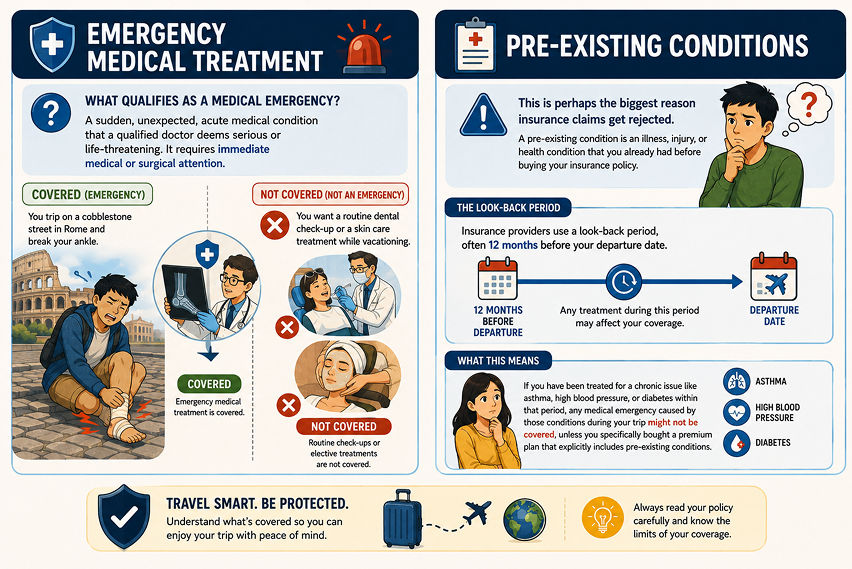

Emergency medical treatment

What qualifies as a medical emergency? Insurance companies define this as a sudden, unexpected, acute medical condition that a qualified doctor deems serious or life-threatening. It requires immediate medical or surgical attention.

If you trip on a cobblestone street in Rome and break your ankle, that is an emergency. If you want to get a routine dental check-up or a skin care treatment while vacationing, that is definitely not covered.

AI-Generated Image

AI-Generated ImagePre-existing conditions

This is perhaps the biggest reason insurance claims get rejected. A pre-existing condition is an illness, injury, or health condition that you already had before buying your insurance policy.

Insurance providers use what is called a look-back period, often 12 months before your departure date. If you have been treated for a chronic issue like asthma, high blood pressure, or diabetes within that period, any medical emergency caused by those conditions during your trip might not be covered, unless you specifically bought a premium plan that explicitly includes pre-existing conditions.

Emergency medical evacuation and repatriation

These sound incredibly dramatic, but they are vital lifesavers.

- Emergency medical evacuation: If you are hiking in a remote mountain area or staying on a secluded island and suffer a severe injury, this benefit covers the transportation cost to the nearest proper hospital, even if that means chartering a helicopter.

- Repatriation of mortal remains: It’s a sad topic, but one we must face. If an insured traveller passes away during a trip, this covers the logistical costs and paperwork required to bring their body back home to the Philippines.

Also Read: Falling ill while travelling? Here's how travel insurance will come to your rescue

3. Travel inconveniences: Delays, losses, and cancellations

Let’s shift to the less dangerous but incredibly annoying disruptions: flight updates and luggage mishaps.

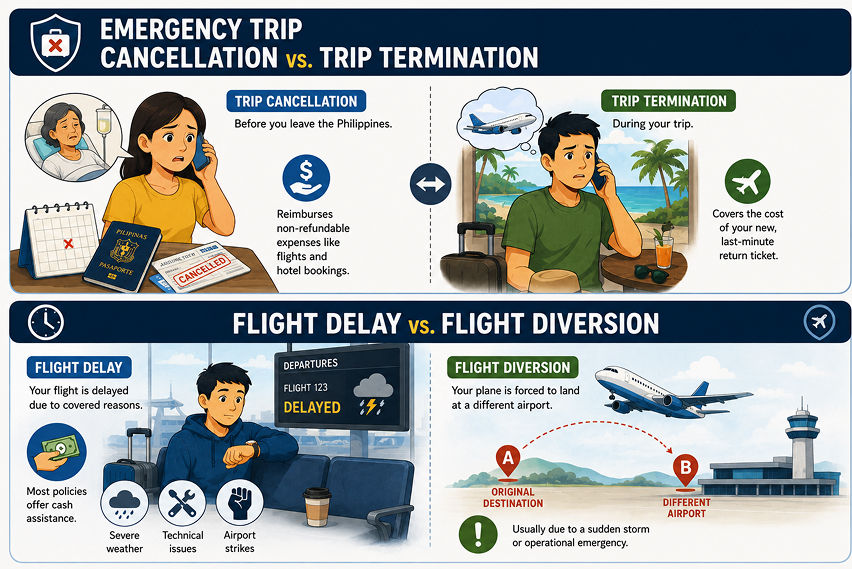

Emergency trip cancellation vs. trip termination

These two terms sound identical, but they apply to entirely different moments of your journey.

Trip cancellation: This happens before you leave the Philippines. If you or an immediate family member falls dangerously ill a few days before your flight, causing you to cancel the whole vacation, this benefit reimburses you for non-refundable expenses like flights and hotel bookings.

Trip termination: This happens during your trip. If you are already enjoying your vacation, but an emergency forces you to cut your trip short and fly back home immediately, this covers the cost of your new, last-minute return ticket.

AI-Generated Image

AI-Generated ImageFlight delay vs. flight diversion

We all know that flight delays are a common headache for Pinoy travellers.

Flight delay: Most policies offer cash assistance. However, the delay must be caused by specific reasons, such as severe weather, technical airline glitches, or airport strikes.

Flight diversion: This occurs when your plane is forced to land at a different airport than originally planned, usually due to a sudden storm or an operational emergency at your destination airport.

Baggage mishaps: Loss, damage, and delay

Your bags go through a lot. When checking your policy, look closely at how "Baggage" is defined. Often, the policy explicitly states that the benefit covers the bag or suitcase itself, as well as clothing and personal effects.

However, there is a big catch: expensive items like laptops, smartphones, luxury watches, and jewellery are usually excluded from standard baggage loss benefits. Those items belong in your carry-on luggage anyway!

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

4. The hidden details: What insurance won’t cover

To truly master travel insurance policy terms, you have to look at what the policy excludes. These are known as General Exclusions.

Extreme sports and adventurous activities

Are you planning to go skydiving in Dubai, scuba diving in Apo Reef, or bungee jumping in New Zealand? Regular travel insurance policies usually exclude these "hazardous activities." If you love high-risk adrenaline rushes, you need to look for a specialised adventure or sports coverage add-on.

AI-Generated Image

AI-Generated ImagePregnancy-related conditions

Travelling while pregnant is perfectly fine, and expectant mothers can buy travel insurance. However, you must know that standard medical benefits usually will not cover expenses arising from pregnancy, childbirth, miscarriage, or abortion.

Also Read: The cost of flying unprotected: Why travel insurance is your true best friend

Step-by-step guide: How to make a successful claim

Knowing the terms is half the battle; knowing how to act when things go wrong is the other half. If you find yourself in a situation where you need to use your insurance, remember these three crucial words: Document everything instantly.

- Notify your insurance provider as soon as possible. Many companies require you to report the incident within 24 to 48 hours of it happening. (Find out what your policy timeline requirements are)

- Get the official report/statement. If your flight is delayed, ask the concerned airline’s authority for an official report or a delay certificate. If you are robbed, go to the local police station and get a physical police report. Without these documents, proving your claim is almost impossible.

- Keep receipts. If your baggage is delayed for several hours and you need to buy basic toiletries and a change of clothes, keep every single receipt. The insurance company will require them to reimburse you.

Note that each insurance company and policy is different, built around a certain set of terms and conditions. So, don’t generalise what is expected of you or what is included & excluded. It is best to give your policy a thorough read; you can always ask your agent for clarification.

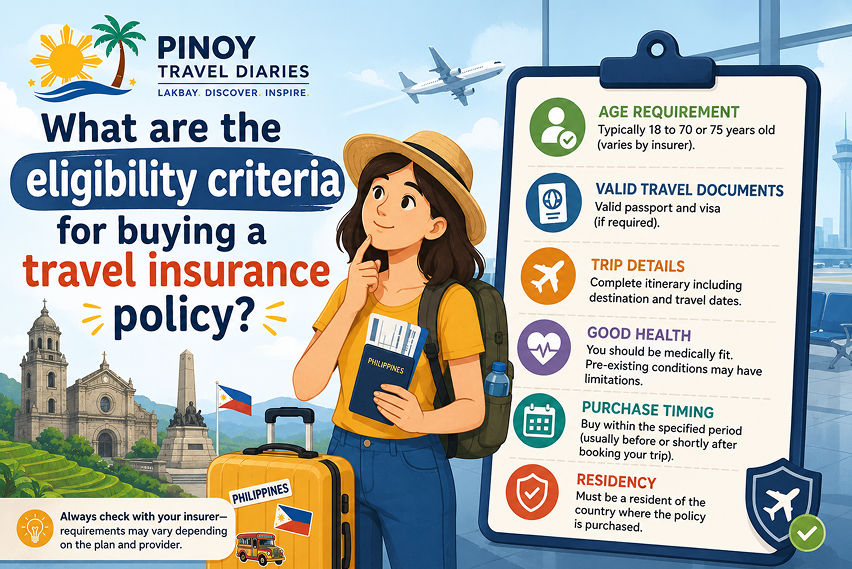

Also Read: What are the eligibility criteria for buying a travel insurance policy?

Bottom line

Travel insurance isn’t just a random piece of paper or a PDF sitting forgotten in your email inbox. It is your financial safety net. By taking just a few minutes to understand the essential terms of your travel insurance policy, you shift your perspective from hoping nothing goes wrong to knowing exactly what to do if you land in trouble.

So, now before you head out for vacation time with friends/family, make sure to have a quick look at your policy - understand the inclusions & exclusions, know the effective dates, and claim requirements. All this will allow you to travel.

Also Read: A complete guide to travel insurance for different travellers

FAQs

Q1. Is it possible to buy travel insurance if my flight departs tomorrow?

Ans. Yes! As long as you purchase the policy before your flight's scheduled departure time from the Philippines, you can buy it online, even the night before your trip. However, it’s always best to buy it as soon as you book your flights so you are protected against unexpected trip cancellations.

Q2. What should I do if the airline loses my luggage?

Ans. First, do not leave the baggage claim area without filing a formal complaint with your airline. Secure a report from the counter. After that, contact your insurance provider’s emergency hotline immediately to notify them of the loss and get guidance on your next steps.

Q3. Are international travel insurance policies valid for domestic trips within the Philippines?

Ans. Usually, no. Insurance plans are categorised separately. If you are travelling locally (e.g., flying from Manila to Siargao), you need to purchase a specific Domestic Travel Insurance plan. If you are going abroad, you must choose an International Plan that covers your specific geographic destination.

Q4. What does a "Look-Back Period" mean for medical conditions?

Ans. A look-back period is the time frame that insurance companies review to determine whether you had any illnesses or medical consultations. If a medical issue arises during this timeframe, it is considered a pre-existing condition and may be excluded from emergency medical coverage.

Q5. Is it possible to extend my travel insurance policy if I decide to stay longer abroad?

Ans. Yes, some insurance companies allow you to extend your policy coverage if you request it before it expires.

Also Read: What’s not covered under a travel insurance policy? A must-read for Filipino travellers