Picture this: You’ve been counting down the days for your dream trip with friends. Your bags are packed with your aesthetic clothes, your itinerary is colour-coded, and you even bought a travel insurance policy just to be safe. You feel completely invincible. Nothing can stop you now, right?

But then, a day before your flight, you suddenly remember a bad toothache you neglected for three months. It gets so painful that you have to cancel the flight to see a dentist. "No worries," you think, "my insurance will handle it." But when you file a claim, the company gives you a polite but firm, "Sorry, request denied."

Wait, what? Aren't insurance policies supposed to protect you from everything bad that happens on a trip?

Also Read: What is travel insurance, and why every Filipino traveller should understand it

Not exactly. While having travel insurance is one of the smartest decisions you can make before exploring the world or going on a domestic trip, it isn’t a magical shield. It is a legal contract with rules, boundaries, and a list of things it simply will not pay for.

Let’s break down exactly what's not covered under a travel insurance policy so you won't get caught off guard on your next adventure.

Also Read: The cost of flying unprotected: Why travel insurance is your true best friend

1. Pre-existing medical conditions

Let’s start with the biggest reason claims get rejected worldwide. Imagine you have asthma, high blood pressure, or a back injury that you’ve been treating for years. If you fly to Europe and have a sudden medical emergency caused by that same condition, your standard travel insurance policy most likely won't cover your hospital bill.

In insurance terms, this is called a pre-existing medical condition. Insurance companies expect you to buy coverage for unexpected, accidental emergencies and not for matters/things you already knew were wrong before you bought the plan. If you need coverage for an ongoing condition, you usually have to declare it beforehand and pay an extra premium for a special medical rider.

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

2. Changing your mind

AI-Generated Image

AI-Generated ImageLife happens. Sometimes, you fight with your travel buddy, you feel too tired, or you suddenly get hit by bad vibes about a destination. Maybe you booked a flight but suddenly realised you'd rather stay home and sleep.

Can you cancel your trip and get a refund? Standard travel insurance says: absolutely not. You cannot claim insurance benefits just because you "changed your mind" or feel sudden travel anxiety. Unless you specifically purchased an expensive add-on, your policy will only pay out if a serious, documented emergency, such as a severe typhoon or an unexpected medical admission, causes your cancellation.

Also Read: Falling ill while travelling? Here's how travel insurance will come to your rescue

3. Adventure lover? You might be on your own

Filipinos are naturally adventurous. We love trying new things when we travel, whether it's skydiving, scuba diving, or renting a scooter to explore the city.

Before you jump out of that plane or rev up that engine, you need to read the fine print. Most standard travel insurance policies completely exclude extreme sports and high-risk activities.

This often includes:

- Bungee jumping, paragliding, and skydiving.

- Scuba diving without a certified license or going past a certain depth.

- Mountain climbing requires professional ropes and equipment.

Furthermore, if you rent a motorbike in Thailand or Siargao and crash, your insurance will likely reject your medical claim if you don't have a valid international driving license or weren't wearing a helmet. Always check if you need to buy an "adventure sports rider" before doing anything wild!

Also Read: Traveller's blueprint: How and when travel insurance pays for emergencies

4. Reckless actions and under the influence of illegal substances

AI-Generated Image

AI-Generated ImageWe all love a good vacation drink. But here is an ugly truth: if you get heavily intoxicated, wander into the street, get hit by a car, or lose your wallet, your insurance company will leave you to handle the mess yourself.

Any accidents, injuries, or losses that happen while you are under the influence of alcohol or recreational drugs are strictly excluded. Insurance is there to protect you from bad luck, not bad decisions.

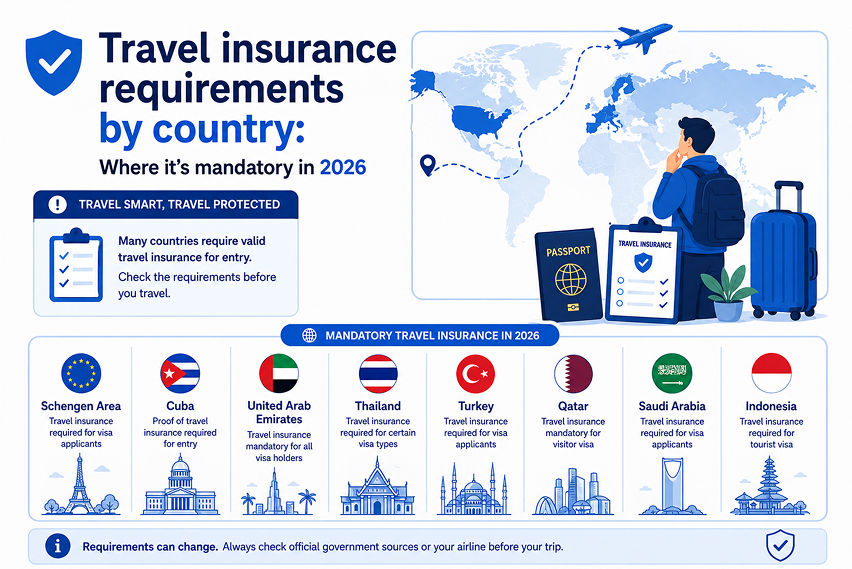

Also Read: Travel insurance requirements by country: Where it's mandatory in 2026

5. Wars, natural disasters, and known events

Living in the Philippines, we are all too familiar with typhoons, earthquakes, and volcanic activities. If a typhoon hits Manila and forces airlines to cancel flights, your insurance will usually cover you; however, it only does so if you bought the policy before the typhoon was officially named and publicised.

If you see a massive storm on the news heading straight for your travel date, and you hurriedly buy travel insurance that afternoon, hoping to get compensated when the flight gets cancelled, you are out of luck. Insurance companies most often do not allow you to buy a policy to cover a house that is already on fire. Similarly, incidents caused by political riots, war, or sudden government travel bans are excluded from standard plans.

Also Read: What does travel insurance actually cover in the Philippines?

6. Valuables left unattended

AI-Generated Image

AI-Generated ImageLosing your baggage due to the airline's misplacement is covered. Having your phone stolen out of your back pocket in a crowded Parisian subway is usually covered, too, provided you get a local police report at the earliest.

However, leaving your expensive DSLR camera or iPhone sitting on a cafe table while you go to the restroom is a completely different story. If your belongings are stolen because they were left unattended in a public space, the insurance company views it as negligence, and your claim will be swiftly denied.

Also Read: Domestic vs. International Travel Insurance: A complete guide for Filipino travelers

Wrapping it up: Travel smart, read the fine print

Does all of this mean travel insurance is a scam? Not at all! Travel insurance is an absolute lifesaver for unexpected medical emergencies, major flight delays, and lost luggage. It has saved thousands of Filipinos from going bankrupt due to overseas hospital stays.

The secret to being a savvy traveller is managing your expectations. Now that you know what's not covered under a travel insurance policy, you can plan smarter, act more responsibly, and pick the exact add-ons you need.

Now, don't just click "Accept Terms and Conditions" unquestioningly. Spend ten minutes reading the exclusions page, and your future self will thank you later!

FAQs

Q1. Can I buy travel insurance while I am already abroad?

Ans. Generally, no. Most regular Philippine travel insurance providers require you to buy the policy before you leave the country. If you buy it while already wandering around, the policy is usually considered invalid.

Q2. Are routine dental check-ups covered during travel?

Ans. No. Standard travel insurance only covers sudden, severe dental emergencies (such as breaking a tooth in an accident or a sudden, agonising infection). Routine cleanings, regular fillings, or pre-planned orthodontic work are never covered.

Q3. What should I do if my travel insurance claim gets denied?

Ans. Do not panic. Read the denial letter carefully and find out the exact reason your claim was denied. If you believe the provider made a mistake, you can file an appeal and, along with it, provide strong documentation to support your point. If that doesn’t help, you can always reach out to the IC (Insurance Commission) for assistance.

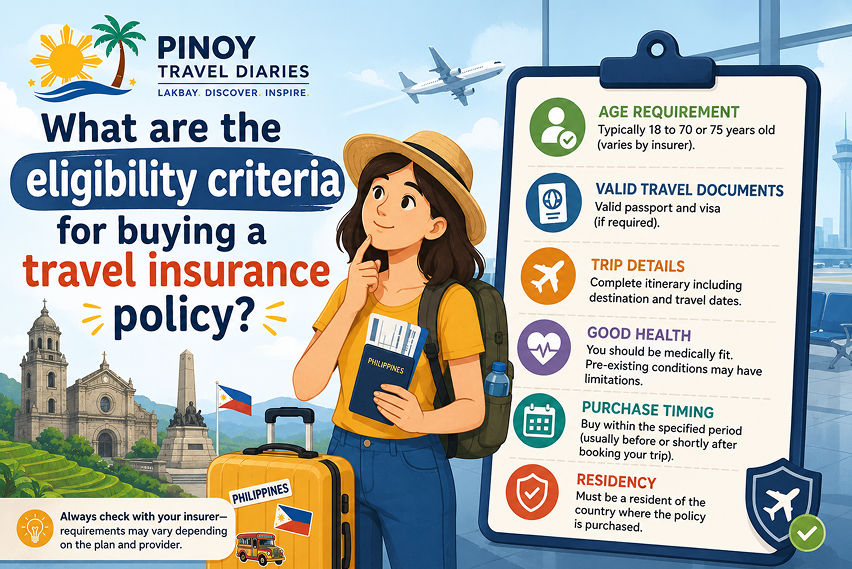

Also Read: What are the eligibility criteria for buying a travel insurance policy?