You have your passport ready, your bags packed, and outfits planned for each day; everything is set. Whether you are counting down the days to see the bright lights of Hong Kong, try the night markets in Taiwan, or just relax on the white sands of Boracay, going on a trip is one of the best feelings ever.

But imagine this: you just landed in Bangkok, and you realise your luggage, which has all your clothes and your camera, is nowhere to be found. Or worse, you suddenly get a terrible stomachache from trying local street food and need to see a doctor immediately.

If you do not have travel insurance, these unexpected moments can instantly turn your dream vacation into an expensive nightmare. Let us look at what can happen if you skip this essential step and why tagging along with an insurance plan is the smartest way to travel.

Also Read: What is travel insurance, and why every Filipino traveller should understand it

Vacation disasters: Expectation vs. Reality

We all want our trips to be perfect. We see beautiful photos on TikTok and Instagram and expect our journey to be just as smooth. However, travel can be unpredictable.

Here is a quick look at common travel problems and how they can hurt your wallet if you are uninsured:

AI-Generated Image

AI-Generated ImageImportant Note: These are everyday examples of what can happen to any traveller. Without a safety net, you are completely on your own to handle the stress and the bills.

Also Read: Travel insurance explained: Medical emergencies, flight delays, and lost baggage

The biggest risks of travelling uninsured

1. Medical emergencies in a foreign country

Healthcare outside the Philippines can be incredibly expensive. In many popular destinations, hospitals will ask you to pay up front before a doctor even looks at you.

If you get a deep cut from hiking, twist your ankle on the street, or get severe dehydration, the bill can quickly empty your bank account. What makes it trickier is that PhilHealth and local Philippine HMOs generally do not cover you when you are outside the country. If you do not have travel insurance, every single pill, doctor's visit, and X-ray will be paid for out of your personal savings.

Also Read: Falling ill while travelling? Here's how travel insurance will come to your rescue

2. Expensive medical transport

What if you are visiting a remote island or a small mountain town and have a serious medical emergency? You might need to be flown to a major city hospital via an emergency helicopter or ambulance.

This service, called medical evacuation, is among the most expensive things that can happen to a traveller. It can cost you hundreds of thousands of pesos. Travel insurance ensures that if you need urgent medical care, the insurance company coordinates and pays for the transport so your family does not have to scramble for money during a crisis.

Also Read: Traveller's blueprint: How and when travel insurance pays for emergencies

3. Flight chaos and lost bookings

Sometimes, the problem starts before you even leave the airport. Airlines can delay or cancel flights due to mechanical issues or bad weather.

If your flight is cancelled and you miss your connecting flight to another country, you could lose the money you spent on your non-refundable hotel rooms. A travel insurance policy protects your wallet by reimbursing you for missed bookings and helping cover the cost of food and a place to sleep while you wait for the next flight.

4. Lost or stolen items

Losing your belongings is incredibly stressful. If someone steals your phone while you are taking photos, or if your passport goes missing, you will have to spend precious vacation time and money fixing the problem. Insurance helps by reimbursing you for your lost items and providing emergency cash or assistance to obtain temporary travel documents from the embassy.

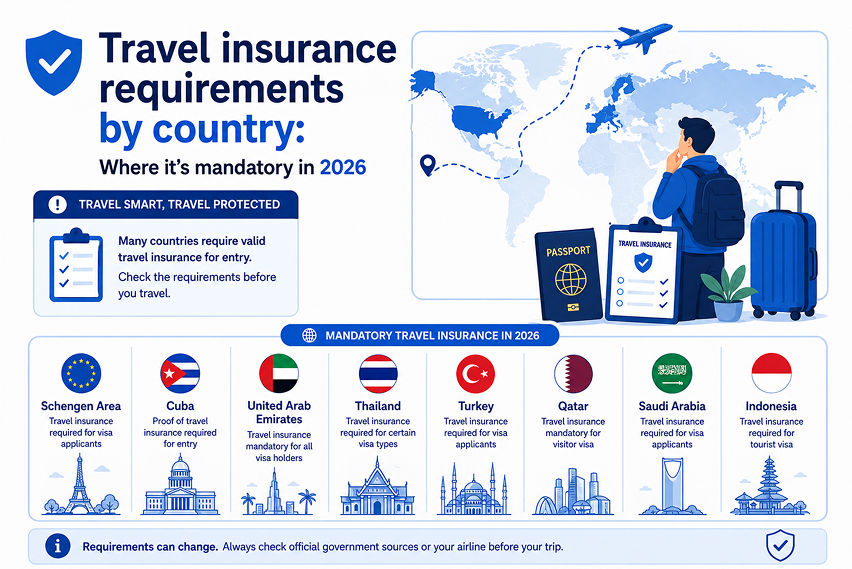

Also Read: Travel insurance requirements by country: Where it's mandatory in 2026

Why do some Pinoy still skip travel insurance?

Even though the risks are high, many travellers still choose to fly without insurance. Here are the most common myths:

- "It costs too much money." In reality, basic travel insurance packages can start for as low as PHP 300.

- "My trip is only for three days." Accidents do not look at your calendar. A bad injury or a cancelled flight can happen the moment you arrive or on the last day.

- "I am a lucky person." It is great to stay positive, but global events, weather changes, and airline mistakes are beyond your control.

Also Read: What does travel insurance actually cover in the Philippines?

Smart travel checklist

Before you head to the airport, make sure you have checked these items off your list:

AI-Generated Image

AI-Generated ImageAlso Read: The most common travel insurance myths Filipinos still believe

Bottom line

At the end of the day, planning a trip should be fun and exciting. You should be thinking about the food you will eat and the memories you will make, not worrying about what will happen if things go wrong. Spending a few hundred pesos on travel insurance gives you an invisible safety shield. If something bad happens, you have an expert team ready to help you and pay for the damages.

Pack your bags, protect your journey, and enjoy your travels with total peace of mind!

Also Read: Domestic vs. International Travel Insurance: A complete guide for Filipino travelers

FAQs

Q1. Will PhilHealth cover my medical bills if I get sick on my trip?

Ans. Only if you are travelling domestically. PhilHealth only covers medical costs inside the Philippines. It will not cover your doctor visits, medicines, or hospital stays when you are travelling in another country.

Q2. Is travel insurance mandatory for international trips?

Ans. It depends on where you are going. Some regions, such as the Schengen area in Europe, require travel insurance before granting a visa. Even if your destination (such as Singapore or Hong Kong) does not require it by law, it is still highly recommended to protect yourself against high costs.

Q3. What should I do if the airline loses my luggage?

Ans. First, go to the airline's baggage claim counter at the airport and report the problem immediately to get a written report. Keep this document safely, as you will need to submit it to your travel insurance provider to claim money for your delayed or lost items.

Q4. Can I still buy travel insurance if my flight is tomorrow?

Ans. Yes! You can easily purchase travel insurance online up to 24 hours before your flight departs. However, it is always best to buy it as soon as you book your flights, so you are protected against unexpected trip cancellations before your vacation even starts.

Q5. I am just travelling to Cebu, do I need travel insurance?

Ans. Yes. Even inside the Philippines, flights can get delayed or cancelled due to sudden typhoons, and luggage can still go missing. Domestic travel insurance is very affordable and protects you against these local travel headaches.

Q6. What happens if I lose my passport while I am overseas?

Ans. If you lose your passport, contact your travel insurance provider's 24/7 hotline immediately. They will guide you on how to contact the nearest Philippine Embassy to get an emergency travel document.

Also Read: Smart travel: Should you buy travel insurance for one trip or the whole year?