After the tragic road accident, you filed an insurance claim with your insurer, thinking that the settlement amount would help with the repair and medical bills. After waiting a month, when you receive the insurer's letter, you open it, expecting a payout that covers those massive bills. Instead, a single word jumps out at you from the letter, that is, DENIED.

Reading this, your stomach drops and your heart skips a beat. And why not? You have been paying your premium on time for years, and the one time you actually wanted to seek policy benefits, your insurer left you alone. It feels like a massive betrayal.

But this is not the end, as most car owners may think. A denial letter is not a final verdict; it is just your provider’s opening offer. Under the Philippines Insurance Code, a policyholder has the legal right to challenge the insurer’s decision.

So, if your car insurance claim gets rejected, don’t panic. Sit down, take a deep breath, grab a cup of coffee, and we’ll walk you through the exact steps to flip that rejection into a payout.

Also Read: 2026 guide for car insurance claim documents - A must-read

Step 1. Decode the denial

Without getting angry or emotional, it is time to act like a detective. Start by reading the denial letter carefully. Find out why exactly your insurer said no.

In the Philippines, providers usually rely on a few excuses to avoid paying the settlement -

- ‘Late notification’ trap: If you waited a week or more to report the accident, your claim could be denied. Most policies require you to give the provider a heads-up within 24 to 48 hours.

- Unauthorised driver clause: Was a friend or relative driving your car at the time of the accident? If they weren’t explicitly authorised or don't have a valid license, the insurer will flag the issue.

- Wear & tear blame: The insurer might say the bumper damage claimed was already there before the crash, so that they won’t entertain it.

Once you can pinpoint the exact excuse of denial, it is time to work on the evidence you need to prove the insurer wrong.

Also Read: 9 shocking total loss coverage myths every car owner should stop believing

Step 2. Build your counter case

AI-Generated Image

AI-Generated ImageIt is not as simple as writing back to your insurer saying, “Please reconsider, I am a good driver”. Rather, you need solid proof that the insurer cannot contradict. Think of it as preparing an evidence kit that is impossible to say no to.

Start by gathering everything you have from the accident scene -

- Official police report or MMDA traffic accident investigation report

- Clean, high-resolution photos of the damage, road conditions, and positioning of the car

- Time-stamped dashcam footage (this is gold, very difficult for insurers to argue over video evidence)

- A detailed, itemised repair estimate from an accredited mechanic

Also Read: Engine protection in car insurance: What Philippine car owners should know

Step 3. Write a killer internal appeal letter

Before you run to a lawyer or a government agency, you need to give your insurer one last chance to do the right thing. This is called an internal appeal.

Keep this appeal letter polite, firm, and factual. Address it directly to their claim manager, state the policy number, lay out the facts of the accident chronologically, and directly counter the reasons for denial.

Give the insurer 15 to 30 days to review your appeal and respond.

Pro tip: If the insurer uses confusing, ambiguous language in the policy that leads to denial (like ambiguous exclusions), there is a beautiful legal concept called contra proferentem. In simple terms, it means that if an insurer uses vague or confusing policy clauses, the law automatically interprets them in favour of the car owner, not the insurance company.

Also Read: Is your current insurance provider still worth it in 2026? Here’s how to tell

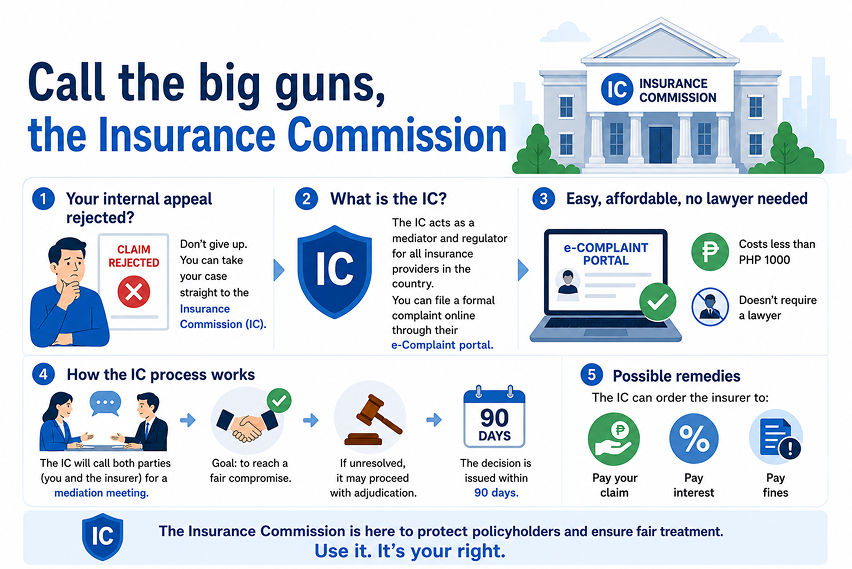

Step 4. Call the big guns, the Insurance Commission

AI-Generated Image

AI-Generated ImageWhat if your provider doubles down and rejects your internal appeal? This is where most car owners would give up and think the only way out is an expensive court case.

But that’s not the case. You can take the case straight to the Insurance Commission (IC).

Do you know the IC acts as a mediator and regulator for all insurance providers in the country? It allows policyholders to file a formal complaint online through their e-Complaint portal. It costs less than PHP 1000 and doesn't require a lawyer.

The IC will start by calling both parties (you and the insurer) for a mediation meeting to see if you can reach a fair compromise. If unresolved, it may proceed with adjudication. The decision is issued within 90 days. As a remedy, IC can order payment from the insurer, and in some cases even interest and fines.

Also Read: Top reasons to choose car insurance with total loss coverage

Bottom line

Appealing a denied claim is not a walk in the park. Instead, the process requires patience, organisation, and a bit of administrative know-how. Also, the entire process can take anywhere from a few weeks to several months, depending on how stubborn your insurer is.

But when you are facing tens of thousands of pesos of repair bills, taking charge and standing on your ground is absolutely worth it. Don’t let a single claim rejection letter intimidate you into believing that you are at fault and need to pay for accident repair bills that should have been covered in the first place.

So, calm that anger, gather evidence, know your rights, and fight for the payout you deserve and have paid for.

Also Read: Car broke down? Here’s how towing can rescue you fast

FAQs

Q1. What is the deadline to appeal a denied car insurance claim?

Ans. When it comes to insurance, time is of the essence. While theoretically the law allows up to 10 years to sue for a written contract, waiting that long doesn’t make sense. Most providers require policyholders to file an internal reconsideration within 30 days of receiving the formal denial letter. In case you are planning to escalate the matter to the IC, you must file an official complaint within one year of the date of claim rejection.

Q2. Can I file a complaint with the IC for any claim amount?

Ans. You can file a complaint for any amount not exceeding PHP 5,000,000. The IC hears, mediates and decides on cases where the actual damage does not exceed the above threshold. In case your claim exceeds this massive sum, you need to file a civil lawsuit directly in court.

Q3. Do I need to hire a lawyer to appeal my denied claim?

Ans. You do not need a lawyer to submit an internal appeal to your insurer. In fact, the IC’s e-Complaint portal is built to be user-friendly for everyday citizens. The IC’s internal process relies on alternative dispute resolution, meaning you can comfortably represent yourself. However, if mediation fails and you decide to take the insurer to a regular trial court, hiring a lawyer who specialises in insurance law is highly recommended.

Q4. What happens if my insurance company simply ignores my claim instead of denying it?

Ans. Insurers cannot legally give you the silent treatment. Under Insurance Commission regulations, insurance companies are mandated to pay valid claims within 30 days after you submit your complete proof of loss and the damage amount is agreed upon

Q5. Will filing an appeal with the Insurance Commission cost me a lot of money?

Ans. Fortunately, no. Escalating a dispute to the Insurance Commission is far more cost-effective than standard court litigation. The filing and administrative fees for an IC complaint are nominal, usually totalling only around PHP 500 to PHP 1,000.

Also Read: Common myths about ‘Acts of Nature’ coverage debunked